A few years ago, I ran a Behavioural Design Sprint for a large European bank. Their challenge: customers weren’t using the savings product the bank had spent eighteen months developing. Beautiful interface, competitive interest rate, frictionless setup. Adoption was below 8%.

The product team assumed it was a marketing problem. The marketing team assumed it was a UX problem. The UX team assumed it was a content problem. Everyone was optimising their own piece of the puzzle, and nobody was asking the one question that mattered: what is the job the customer is trying to get done at the moment of decision? What are they actually trying to achieve in their life when they consider opening a savings account?

This pattern repeats itself across financial services. I see it at pension funds where clients understand the retirement projection and still don’t increase their contribution. At investment platforms where customers log in once, see market volatility, move everything to cash, and never return. The financial sector has built its entire model on an assumption about human behaviour that behavioural science disproved decades ago: give people the right information and they will act in their own financial interest.

The missing variable is not information. It is human behaviour. And the discipline that addresses it is called behavioural design.

Behavioural design for financial services applies behavioural science to close the gap between financial knowledge and financial action. Instead of assuming customers are rational decision-makers, it maps the psychological forces that drive financial behaviour. Using the SUE | Influence Framework©, banks, insurers, investment firms, and fintechs redesign products, onboarding journeys, and customer communications to work with human psychology, not against it.

The numbers behind the financial behaviour gap

The job customers want done: the real starting point

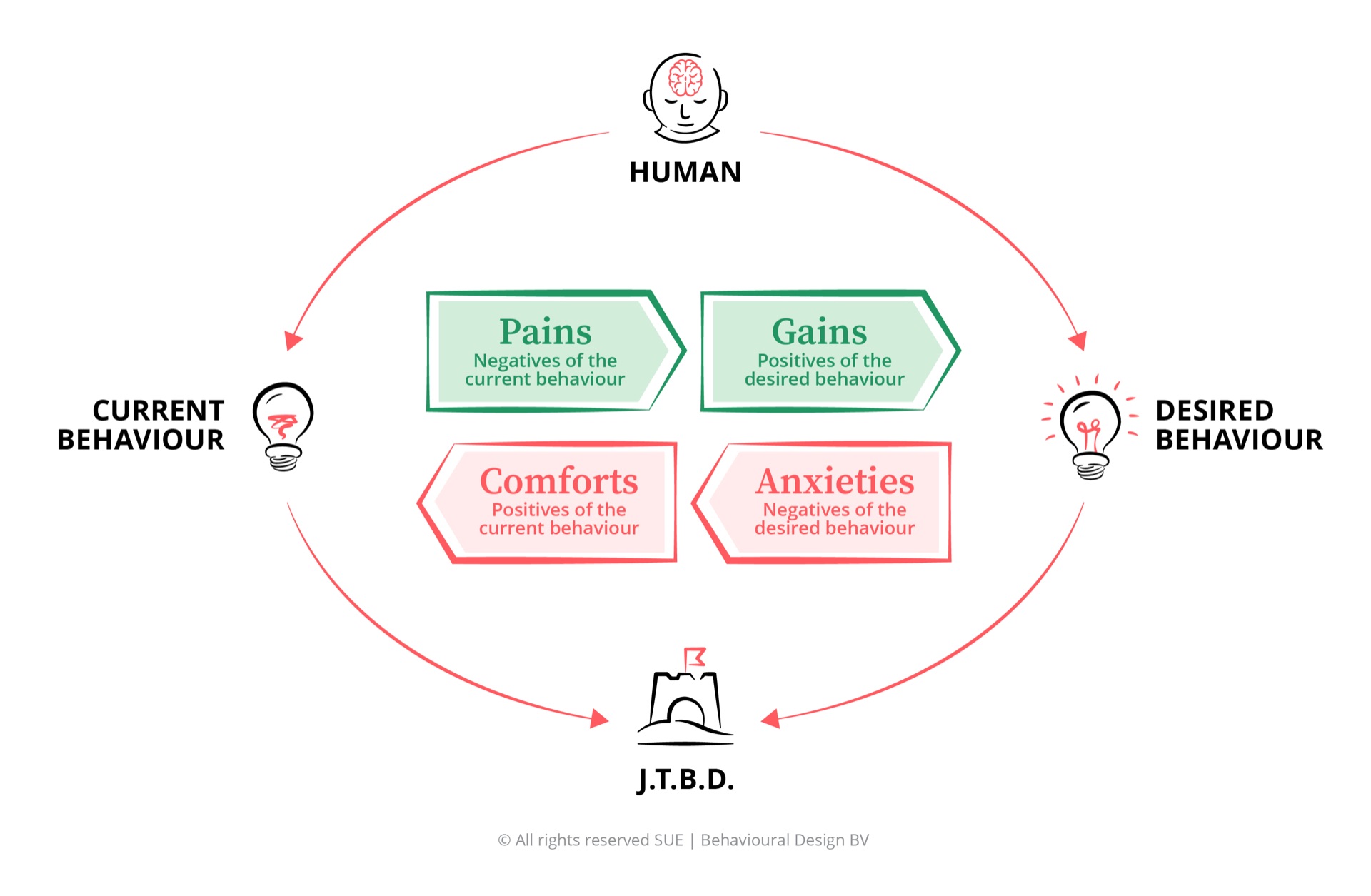

If you ask customers what they want from a bank, they say “a good interest rate” and “low fees.” If you watch what they actually do, you see something different. They want to feel financially safe. They want to reduce anxiety about an uncertain future. At major life moments, buying a home, having a child, planning for retirement, they want to feel in control and not be caught off guard.

Clayton Christensen called this the Jobs to Be Done framework: people hire products to get a job done in their life. A savings account is not hired for the interest rate. It is hired to remove the anxiety of having nothing to fall back on if something goes wrong. A pension product is not hired for tax optimisation. It is hired to create the feeling that your future is sorted, so you don’t have to think about it anymore.[5]

This distinction is not a marketing detail. It is the foundation of every effective behavioural design in financial services. If you don’t understand the job, you design for the wrong moments, solve the wrong friction, and address the wrong emotions. The bank that raised its interest rate and saw adoption increase by 0.4% had not understood the job. The customer didn’t want more interest. The customer wanted security on autopilot.

“What people say and what people do are two fundamentally different things.”

The Art of Designing Behaviour (2024)

Why financial services needs behavioural design

Financial services operates on an assumption that sounds reasonable but is empirically wrong: that customers who have access to good financial information will make good financial decisions. This is the rational actor model. It assumes that people weigh future costs and benefits, calculate expected value, consider risk appropriately, and act in their own long-term interest.

That person does not exist.

What does exist are people who know they should be saving for retirement but experience that necessity as remote, abstract, and deferrable. People who understand diversification but sell their equity portfolio when markets fall 15% because the pain of watching the number go down is unbearable. People who intend to transfer their savings to a higher-interest account and have been intending to do so for three years. These are not failures of knowledge. They are predictable consequences of how the human brain processes financial decisions.

Financial decisions are driven by System 1 thinking: fast, automatic, emotionally loaded, and profoundly influenced by how choices are presented. Financial services products and communications are almost exclusively designed for System 2: slow, deliberate, analytical reasoning. The industry keeps building better calculators for people who are not doing calculations.

Customers don’t fail to engage with financial products. Financial products fail to account for how customers actually make decisions.

This is what behavioural design does: it starts from the empirically accurate model of human behaviour. Not the rational actor, but the actual person. Driven by habits, shaped by defaults, moved by immediate emotions more than future consequences, and profoundly influenced by social context. As I write in The Art of Designing Behaviour (2024): “The goal is not to think about behaviour, but to design for it.” You cannot educate people into better financial behaviour. But you can design it.

Three financial services challenges that behavioural design solves

Challenge 1: the savings product nobody uses

A retail bank had an excellent savings product. Competitive interest rate, no fees, fully flexible. The product team had done everything right: clear product page, targeted email campaign to eligible customers, a streamlined three-click sign-up process. After six months, uptake was 4.7%. The team concluded the interest rate was not competitive enough and raised it. Uptake reached 5.1%.

The interest rate was not the problem.

The product had been designed for a rational customer who would evaluate the offer, recognise the value, and take action. But the actual customer was subject to present bias: saving means giving up spending now for a benefit that arrives years in the future, and the brain systematically discounts future rewards in favour of present ones. The product was also opt-in: customers had to actively choose to start saving. Inaction defaulted to not saving. And inaction is always the most popular choice.

Bank of America illustrates what happens when you flip the default. Their Keep the Change programme automatically rounded every debit card transaction up to the nearest dollar and moved the difference to a savings account. No opt-in required, no salary increases needed, no behaviour change asked of the customer. The result: 12.3 million customers participated, the programme helped customers collectively save over $2 billion, and retention was 99%.[6] The product was not better. The default was different.

Challenge 2: the risk assessment that backfires

An investment platform required new customers to complete a risk assessment before accessing investment products. This was good regulatory practice, designed to ensure customers were matched to products appropriate for their risk tolerance. The problem: 68% of customers who completed the risk assessment selected the lowest possible risk category. The result was a portfolio allocation so conservative that, after inflation, most customers were experiencing a real-terms loss.

The risk assessment was triggering loss aversion at exactly the wrong moment. Questions like “How would you feel if your portfolio fell 20%?” activated the emotional weight of potential loss. The framing of the assessment focused customers on what they could lose rather than what they stood to gain. And because the assessment was presented at a high-anxiety moment (new account, unfamiliar platform, real money at stake), System 1 defaulted to the most conservative option available.

The outcome was regulatory compliance that produced demonstrably worse financial outcomes for customers. Kahneman and Tversky documented this mechanism in 1979: the pain of loss weighs psychologically twice as heavily as the joy of equivalent gain.[3] Build a risk assessment that keeps returning to potential loss and you have built an anxiety machine.

Challenge 3: the onboarding that loses 40% of customers

At SUE we worked with a large insurance company that wanted to improve its digital onboarding conversion. The technical funnel was clean. The products were competitive. Yet 40% of potential customers dropped off somewhere in the sign-up process, with the identity verification step as the biggest exit point. The product team’s instinct was to make verification faster.

But speed was not the problem.

Customers were abandoning because onboarding asked them to make a series of micro-decisions under conditions of low trust and high ambiguity. The journey had been designed sequentially: first create your account, then verify your identity, then choose your product type, then set up your preferences. Each step felt like a separate commitment. Customers repeatedly reached points where they were unsure what they were committing to, whether their data was safe, and how much more of this there was.

In behavioural terms: friction had accumulated to the point where the perceived cost of continuing exceeded the perceived value of the product. And because the product’s value was still abstract at this point in the journey, the balance was easily tipped. “Simplicity eats willpower for breakfast,” as we write in The Art of Designing Behaviour. Every additional step eats into the customer’s mental energy until they drop off and intend to return later. Later is where intentions go to die.

Influence Framework analysis: what drives and blocks financial behaviour

The SUE | Influence Framework© always starts with the job: what is the customer trying to get done in their life? In financial services, the dominant jobs are financial security (the feeling that things will be okay even if something goes wrong), peace of mind at major life events (mortgage, retirement, inheritance), and control (the feeling of having the situation in hand, even when markets move). Only when you understand the job do you understand which Pains and Gains actually drive behaviour, and which Comforts and Anxieties block it.

Why customers don’t act on financial decisions despite understanding them

Financial services communication addresses the driving forces competently. Customers understand the pension gap, the power of compound interest, the risk of inflation eroding savings. What remains unaddressed are the blocking forces: money habits that run on complete autopilot, and the deep anxiety that financial decisions are high-stakes, irreversible, and can go badly wrong.

Financial anxiety is real and growing: Many customers are aware that they are not saving enough, not invested appropriately, or not prepared for retirement. This creates genuine worry. The pain is there. But it is future-oriented, diffuse, and easy to suppress with the simple decision to think about it later. Fintech marketing exploits this anxiety effectively. The product then gives the customer insufficient reason to convert that intention into action right now.

Life events create moments of urgency: Marriage, a first child, a mortgage, redundancy, inheritance: these moments activate financial concern sharply. Customers in these moments are genuinely motivated to act. These are the highest-leverage intervention points in the customer journey. Any financial product that delivers a feeling of security as a concrete solution at these moments, rather than as an abstract product, will outperform campaigns by a wide margin.

Peer comparison activates discomfort: Discovering that colleagues or friends have pension pots significantly larger than yours, or that peers own property while you rent, creates social pain that can override inertia. Social comparison is one of the strongest activators of financial behaviour change, particularly when it is specific and personal rather than statistical and general.

Financial security as a life goal: Most people genuinely want financial security for themselves and their families. This is a real and powerful gain. The problem is that it is distant, abstract, and has no emotional immediacy for System 1 processing. Compound interest over thirty years is intellectually compelling but emotionally inert. Only when you translate compound interest into “how much more you can spend each month if you stop working at 65” does it become a real motivator.

Ownership and control: Building wealth creates a sense of agency and control over one’s own future. This is motivating for customers who have already started. It is abstract for those who have not. The job is not just ‘building wealth’; it is ‘feeling in control of the future.’ Any product that delivers that feeling earlier and more concretely in the journey wins the customer’s trust.

Tax advantages and employer matching: Concrete, immediate, calculable gains from pension contributions, especially employer matching, are among the strongest motivators available. When customers understand they are leaving “free money” on the table by not enrolling, action rates increase significantly. This is one of the few financial communications that speaks directly to System 1.

Money habits run on complete autopilot: The way people manage money, where it goes, what they spend it on, how much they save, is almost entirely habitual. Most customers spend what arrives in their account in a pattern established years ago and never consciously revisited. This habit system operates below conscious awareness. Asking people to change financial behaviour means asking them to override a deeply embedded System 1 routine with a deliberate System 2 decision. That is a very high cognitive demand. The only effective response is to replace the habit, not to persuade the person.

The current situation feels fine enough: Status quo bias is the dominant force in financial services. The current bank, the current savings rate, the current investment approach: all of them persist not because they are optimal but because changing requires effort and the current situation feels acceptable. “Good enough” is the enemy of better financial decisions. Any financial product that requires a switch must demonstrate that the cost of switching is lower than the pain of staying.

Deferral feels safe: “I’ll sort my pension next year when I earn more” is a comfort. It removes the anxiety of a decision that feels complex and irreversible without requiring any immediate action. Present bias and status quo bias combine to make deferral the default position for a significant majority of working adults.

Financial decisions feel high-stakes and irreversible: Unlike most daily choices, financial decisions feel consequential. A wrong investment decision, a poor pension choice, a bad mortgage: these feel like mistakes that could follow you for decades. This perception of irreversibility creates anxiety that triggers avoidance rather than action. The more a financial product communicates its long-term importance, the more anxious customers become about getting it wrong, and the less likely they are to decide at all.

Loss aversion makes every financial choice feel like a potential loss: Loss aversion means the emotional weight of “what if this goes wrong?” is approximately twice as heavy as the emotional pull of “what if this goes right?” Every investment product, every pension contribution, every financial commitment is experienced through this asymmetric emotional lens. Financial communications that emphasise potential gains cannot overcome the anxiety of potential loss. They barely register.

Complexity creates cognitive avoidance: Financial products are genuinely complex. When complexity exceeds the customer’s ability to evaluate a decision confidently, the brain defaults to inaction. Not because the customer is lazy, but because taking an action you don’t fully understand on something that feels high-stakes is genuinely threatening. The industry’s solution has been to provide more information. The result has been more complexity and less action.

The key insight: Financial services communication overwhelmingly targets the driving forces: calculate the pension gap, show the compound interest chart, explain the product benefits. But customer behaviour is determined by the blocking forces, which operate below the level of rational argument. The comfort of automatic money habits and the anxiety about irreversible financial mistakes are not overcome by better product pages. They are overcome by redesigning the financial journey so the desired behaviour is the default, the easiest choice, and the one that requires no decision at all.

Five behavioural interventions for financial services

-

Default-optimise savings products (SPARK - C01 Default)

The single most powerful intervention available to any financial services organisation is the default. When saving is opt-out rather than opt-in, participation rates increase dramatically. This is not manipulation; it is design that works with the grain of human behaviour rather than against it. Customers retain full control: they can change or cancel at any moment. But the default exploits the most reliable fact about human behaviour: inaction is always the most popular choice. Design inaction to produce the financial outcome you want for your customer. Save More Tomorrow by Thaler and Benartzi shows that the same principle works for future commitments: ask customers not to save more now, but to commit today to saving from their next pay rise. Savings rates quadrupled.[9]

-

Frame financial communication around loss, not gain (WANT - W05 Loss aversion)

Because of loss aversion, “You are losing £347 per month in retirement income by not increasing your contribution now” is considerably more motivating than “Increase your contribution and gain £347 more per month in retirement.” This is the same information. The framing is different. Financial communications, pension dashboards, and investment product descriptions should be systematically reviewed through the lens of loss framing. This is not scaremongering; it is accurate communication of what is actually happening when customers underinvest. Research on health screening found that loss-framed materials increased participation by 12% over six months.[10] The same mechanism applies to financial communication.

-

Reduce friction in digital onboarding (CAN - C02 Option reduction)

Every additional step in a financial onboarding journey is a drop-off risk. Every choice that requires genuine deliberation is a potential exit point. The goal is not to make onboarding faster; it is to reduce the cognitive load at moments of high anxiety. Set sensible defaults for every optional preference. Separate the minimal viable account creation from the fuller setup process. Make the value of the product tangible before asking for identity verification. Show customers how many steps remain. Design onboarding as if your customer is simultaneously doing something else, because they almost certainly are. “Influence is far more judo than karate,” as we write in our book: work with the energy flows already present, don’t fight them head-on.

-

Build financial micro-habits through small commitments (AGAIN - C13 Endowed Progress)

Large financial commitments activate the full anxiety of irreversibility. Small ones do not. The round-up model is effective not because the amounts are significant but because it builds the habit of saving with no single decision that feels consequential. Nunes and Dreze showed that a feeling of progress on a goal significantly increases completion rates: if customers feel they have already started, they are far more likely to continue.[11] Use annual pension contribution reviews as a default touchpoint, pre-loaded with a suggested increase that requires only one click to confirm. Habit formation in financial behaviour requires the same conditions as in any other domain: small steps, consistent triggers, and visible progress.

-

Use social proof in investment communications (WANT - W01 Social proof)

Customers are powerfully influenced by what they believe their peers are doing financially. “Customers with a similar profile to yours have on average £280 more in their savings account” activates the social comparison that is one of the strongest drivers of financial behaviour change. Displaying peer benchmarks in banking apps, pension dashboards, and investment portals normalises higher savings rates and more active investment behaviour. This works precisely because it bypasses the rational deliberation that financial communications typically try to trigger, and instead activates the System 1 drive to conform to perceived social norms. As I write in The Art of Designing Behaviour: “People don’t resist change. They resist being changed.” But if change is the norm among people like them, it is no longer something being done to them.

Which cognitive biases matter most in financial services

Financial decisions are among the highest-stakes choices people make, and they are shaped by cognitive biases operating well below the level of rational deliberation. Here are the five biases with the most impact on customer financial behaviour and financial services product design.

Loss aversion

The pain of losing £500 feels twice as strong as the pleasure of gaining £500. In financial services, this drives poor investment timing, excessive conservatism in risk assessments, and the decision to hold losing positions too long rather than realise the loss.

Read the full analysis → Behavioural DesignAnchoring bias

The first number a customer encounters in a financial context becomes the reference point for all subsequent judgements. The original purchase price of an investment anchors the customer’s sense of whether they are “up” or “down,” distorting every future decision about that asset.

Read the full analysis → Behavioural DesignStatus quo bias

Customers keep the same current account for an average of seventeen years, despite switching incentives worth hundreds of pounds. Status quo bias is the dominant force in financial services: the current product persists not because it is optimal, but because changing requires effort.

Read the full analysis → Behavioural DesignPresent bias

Retirement is thirty years away. The pain of a smaller pay cheque this month is immediate. Present bias explains why customers consistently undersave despite understanding the consequences: the future benefit of saving is systematically discounted against the immediate cost of not spending.

Read the full analysis → Behavioural DesignFraming effect

“Your pension will replace 40% of your final salary” and “Your pension will leave you with a 60% income shortfall at retirement” describe the same situation. Customers respond very differently. How financial information is framed determines whether it triggers anxiety, action, or avoidance.

Read the full analysis →Frequently asked questions

How does behavioural design apply to banking?

Behavioural design for banking maps the psychological forces that determine whether customers open savings accounts, complete onboarding flows, engage with investment products, or plan for retirement. Instead of relying on financial literacy campaigns, it redesigns the decision environment: product defaults, communication framing, onboarding friction, and digital interfaces. The SUE | Influence Framework© diagnoses the specific Comforts keeping customers in their current financial habits and the Anxieties blocking engagement, then applies SWAC interventions at the moments where financial behaviour actually happens.

Can behavioural design improve savings rates?

Yes. Under-saving is primarily a behavioural problem, not a knowledge problem. Customers know they should save more. They don’t because of present bias, status quo bias, and the simple friction of having to make an active decision. The most effective intervention is the default: making saving automatic so that inaction produces saving rather than spending. Bank of America’s Keep the Change programme reached 12.3 million customers and helped them collectively save over $2 billion, purely by making saving the default outcome of every transaction. Studies of opt-out pension enrolment show participation rates consistently above 90%, versus below 50% for opt-in designs.

What is the difference between behavioural finance and behavioural design?

Behavioural finance describes and explains the cognitive biases that lead to irrational financial decisions. It is primarily diagnostic. Behavioural design uses those insights to change the environment so better financial decisions become easier, more natural, and more automatic. Behavioural design is the applied, interventional discipline. It doesn’t just name the bias; it redesigns the product, process, or communication so the bias works for the customer rather than against them. The question of behavioural finance is ‘why do people behave this way?’ The question of behavioural design is ‘how do I design an environment where better behaviour is the path of least resistance?’

How does loss aversion affect investment decisions?

Loss aversion means people feel the pain of a financial loss approximately twice as strongly as the pleasure of an equivalent gain, as Kahneman and Tversky established in Prospect Theory in 1979. In investment contexts, this leads to selling assets during market downturns, holding underperforming investments too long, and avoiding investment altogether. Behavioural design addresses this by reframing investment communications around avoided losses, reducing the frequency with which customers see portfolio fluctuations, and redesigning risk assessment conversations to focus on long-term goals rather than short-term scenarios.

Why do financial literacy programmes fail?

Financial literacy programmes fail because they operate on a false premise: that people make poor financial decisions because they lack information. Fernandes et al. analysed more than 200 literacy programmes and found that fewer than 0.1% of participants measurably improved their long-term financial behaviour. Financial behaviour is driven by System 1 thinking: automatic, emotional, habit-driven. Financial literacy addresses System 2: deliberate, analytical, slow. You cannot change System 1 behaviour with System 2 arguments. What works is redesigning the financial environment so the desired behaviour is the default, the easiest, and the most socially normal option. That is behavioural design.

PS

I’ve worked with financial services organisations for over a decade, and the frustration is always the same. Excellent products, rigorous compliance, well-funded communications campaigns. And customers who still don’t save enough, still don’t engage with their investments, still put off their pension planning until next year. At SUE, our mission is to help organisations close exactly this gap: the space between what customers intend and what they actually do. Start from the job your customer is trying to get done. Understand the blocking forces that your product has never addressed. And make the right behaviour the default. The financial sector doesn’t need more financial education. It needs better design. The principles behind that are what we describe in the SUE | Influence Framework and in The Art of Designing Behaviour (2024).