Imagine a pension scheme where employees have to actively decide whether to participate. On average, around 30 percent enrol. Now change the default so that everyone is automatically enrolled unless they actively opt out. Participation rises to 90 percent. Same scheme, same people, same information. Only the structure of the choice has changed.

This is behavioural economics in practice. And it is precisely this kind of insight that produced two Nobel Prizes and transformed an entire discipline.

Behavioural economics is the field that studies how psychological, social and emotional factors influence people's economic decisions. It challenges the rational actor model of classical economics and shows that people act in systematically predictable irrational ways. Key figures: Kahneman, Tversky, Thaler, Ariely. Behavioural economics provides the scientific foundation on which behavioural design builds its methodology.

What is behavioural economics?

Classical economics is built on an attractive but fundamentally incorrect model of the human being: the homo economicus. This fictional creature rationally weighs all available information, has consistent preferences, always maximises its own utility and is not influenced by irrelevant factors such as how a question is framed or what others are doing.

The problem: real people never do this. They are driven by emotions. They are lazy in processing information. They choose the easiest option rather than the best one. They respond strongly to the way choices are presented. And they are deeply attached to the status quo.

Behavioural economics began in the 1970s as a systematic attempt to understand how people actually make decisions, rather than how they theoretically should. It combined the rigorous methods of economics with the empirical insights of psychology. The result was a field that proved both scientifically robust and practically revolutionary.

People do not act irrationally in a random way. They act irrationally in a systematically predictable way. That is the point.

The key figures and their contributions

The history of behavioural economics begins with a friendship. Daniel Kahneman, an Israeli psychologist at the Hebrew University of Jerusalem, met Amos Tversky in the early 1970s. Together they began a series of brilliant experiments that undermined the foundations of rational choice theory.

In 1979 they published Prospect Theory: An Analysis of Decision under Risk.[1] This paper, published in the economics journal Econometrica, is considered one of the most cited papers in the social sciences ever. The core finding: people weigh losses psychologically more heavily than equivalently large gains. A loss of £100 feels larger than a gain of £100. This seems simple but it explains an enormous range of economic behaviour that the classical model could not account for.

Kahneman received the Nobel Prize in Economics in 2002, the first psychologist to do so. Tversky had died in 1996; otherwise they would undoubtedly have shared it.

Richard Thaler, who for years was regarded as an odd duck in the economics world, built on the work of Kahneman and Tversky. He developed the concept of mental accounting: people divide money into mental buckets with different rules, rather than treating all their money as fungible. He introduced together with Cass Sunstein the concept of the nudge: small pushes that steer people towards better choices without restricting their freedom.[2] In 2017 Thaler received the Nobel Prize in Economics.

Dan Ariely, professor at Duke University, made behavioural economics accessible to a broad audience with his book Predictably Irrational (2008). His experiments show how irrational human behaviour is nevertheless systematic and predictable. Robert Cialdini, social psychologist, documented the six principles of social influence that to this day form the basis of persuasion strategy worldwide.

The core concepts you need to know

Prospect theory and loss aversion

The most fundamental insight of behavioural economics: people are loss averse. The pain of losing something is psychologically approximately twice as large as the pleasure of gaining an equivalent object. This has far-reaching consequences for how you design policy, products and communications. Framing a subscription as “don’t miss any benefit” works differently from “enjoy all the benefits,” even though you are communicating exactly the same thing.

Bounded rationality

Herbert Simon introduced in the 1950s the concept of bounded rationality: people do not strive for the maximum but for the satisfactory. They stop searching as soon as they find an option that is good enough. They use heuristics (mental rules of thumb) rather than full information processing. This is not stupid. It is efficient. But it makes people systematically susceptible to certain kinds of errors and manipulation.

Mental accounting

People do not treat money as fungible. A bonus feels different from a salary. Holiday pay feels different from savings. Money found on the street is spent more readily than money you worked hard for. Thaler’s concept of mental accounting explains why people make financially irrational decisions while feeling completely rational.

Present bias

People overestimate the importance of the present and underestimate the future. They would rather have £10 now than £15 in a week, even though that is financially irrational. This is at the core of almost every long-term behaviour problem: saving, eating healthily, sustainable investment. The future benefits are too abstract and the present costs too concrete.

Three practical applications

Pension saving: the power of defaults

The pension example at the start of this article is not a hypothetical scenario. It is one of the most replicated findings in applied behavioural economics. Shlomo Benartzi and Richard Thaler developed the Save More Tomorrow programme, in which employees could agree in advance to automatic increases in their pension contributions with every pay rise. The result: participants increased their savings rate from 3.5 to 13.6 percent over 40 months. No coercion, no financial advice, just smart design of the choice environment.

Healthcare: framing and loss aversion

Doctors and public health professionals have been struggling for decades with adherence. Patients forget medications, skip check-ups and do not follow advice. Behavioural economics provides an explanatory framework and concrete tools. Messages framed as loss (“If you skip this screening, you miss the chance to detect cancer at an early stage”) are demonstrably more effective than gain-framed messages. Implementation intentions and commitment devices significantly increase adherence.

Organisations: choice architecture and behavioural design

Many organisational problems that are addressed with communication, training or regulation can be solved more effectively by redesigning the choice environment. Cafeterias that place healthy choices more prominently increase the consumption of healthy food without banning anything. Forms with opt-out rather than opt-in for sustainable options increase participation. Feedback that is socially compared (“84% of your colleagues already recycle”) is more powerful than abstract normative appeals.

Behavioural economics versus behavioural design: what is the difference?

This is the question I get most often. And the answer is less complicated than it seems.

Behavioural economics is a science. It describes and explains how people actually make decisions. It generates empirical knowledge about human behaviour in economic contexts. It is descriptive and explanatory in nature.

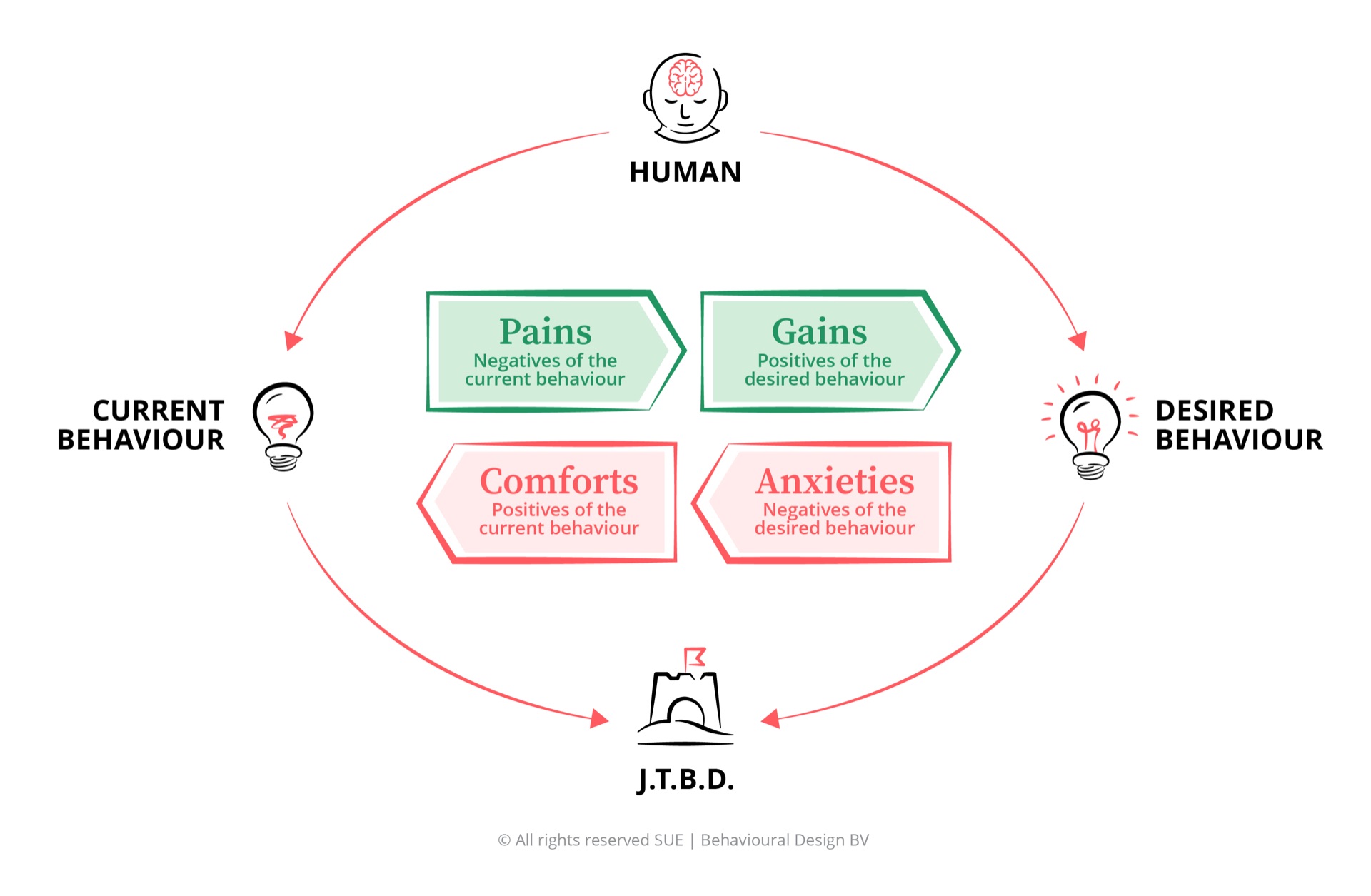

Behavioural design is a methodology. It uses that scientific knowledge to design environments, products, services and communications that facilitate desired behaviour. It is prescriptive and creative in nature. It asks the question: how can we, armed with insights from behavioural economics and related disciplines, design environments in which people more easily make choices that are good for them?

Behavioural economics provides the ingredients. Behavioural design provides the recipe and the kitchen. The SUE Influence Framework is our primary methodological tool: it makes the four forces visible that determine why people do what they do and what holds them back from changing.

Frequently asked questions

What exactly is behavioural economics?

Behavioural economics is the field that studies how psychological, social and emotional factors influence people’s economic decisions. It combines insights from psychology with economic models and challenges the classical image of the rational actor. People do not always act in their own interest, are limited in their information processing capacity and are strongly influenced by the context in which decisions take place.

What is the difference between behavioural economics and classical economics?

Classical economics assumes that people are rational actors who always make decisions that maximise their own interest, have access to all relevant information and have consistent preferences. Behavioural economics shows that none of these assumptions always hold. People are boundedly rational, limited in willpower and boundedly self-interested. They are strongly influenced by framing, defaults, anchoring and social norms.

What is prospect theory?

Prospect theory, developed by Kahneman and Tversky in 1979, describes how people make decisions under uncertainty. The core finding: people weigh losses more heavily than equivalent gains. A loss of £100 feels emotionally larger than a gain of £100. This explains why people show irrationally risk-averse behaviour with potential gains but risk-seeking behaviour with potential losses.

Who are the key figures in behavioural economics?

The most influential figures are Daniel Kahneman and Amos Tversky (prospect theory and heuristics), Richard Thaler (mental accounting, nudge theory, Nobel Prize 2017), Dan Ariely (predictably irrational behaviour) and Robert Cialdini (social influence). Kahneman received the Nobel Prize in Economics in 2002, the first psychologist to do so.

What is the relationship between behavioural economics and behavioural design?

Behavioural economics provides the scientific foundation: it describes and explains how people actually make decisions. Behavioural design is the applied methodology: it uses those insights to design environments, products and communications that facilitate desired behaviour. Behavioural economics is the science, behavioural design is the toolkit.

Conclusion

Behavioural economics is not an esoteric academic discipline. It is a practically powerful scientific lens that explains why people do what they do, even when that is not in their rational interest. And that explanation opens the door to better interventions, better policy designs and better products.

Want to learn how to translate insights from behavioural economics into concrete behavioural design interventions? In the Behavioural Design Fundamentals Course you learn to use the Influence Framework and the accompanying toolkit to systematically analyse and influence behaviour. Rated 9.7/10 by 10,000+ professionals.

PS

At SUE our mission is to use the superpower of behavioural psychology to help people make positive choices. Behavioural economics is the scientific foundation for that. But science alone changes nothing. The combination of scientific knowledge with creative design and systematic methodology is what makes real behaviour change possible. That is precisely what behavioural design provides.