There’s a question I always ask when we start a Behavioural Design Sprint for an insurer: ‘What percentage of your customers are adequately covered?’ The room goes quiet. Not because they don’t know the answer. Because the answer is embarrassing.

In every insurance company I’ve worked with, the same pattern emerges. Customers underinsure their most valuable assets. They delay filing claims until a minor issue becomes a major payout. They let policies lapse at renewal despite being satisfied with the service. The actuarial models are brilliant. The risk assessments are precise. And customer behaviour makes a mockery of both.

The instinct is always to fix the product: better pricing, clearer policy documents, simplified claims processes, digital self-service portals. And it helps, marginally. But the gap between what insurance products offer and how customers actually behave isn’t a product gap. It’s a behaviour gap.

The missing variable is not the product. It is human behaviour. And the discipline that addresses it is called behavioural design.

Behavioural design for insurance applies behavioural science to how people perceive risk, make coverage decisions, and interact with claims processes. Instead of building better risk models, it maps the psychological forces that drive insurance behaviour. Using Job-to-be-Done analysis and the SUE | Influence Framework©, insurers redesign customer journeys, from onboarding to renewal, to work with human psychology rather than assuming customers behave like rational actuaries.

The numbers behind the insurance behaviour gap

What job-to-be-done insurance actually needs to fulfil

Clayton Christensen, the Harvard Business School professor who popularised the concept of job-to-be-done, had a simple theory: people don’t buy products. They hire them to do a job.[5] If the product does the job well, they hire it again. If it doesn’t, they fire it and hire something else.

What job do customers hire insurance to do? This is the question the insurance industry almost never asks. And the answer is more varied than the sector tends to assume.

Customers hire insurance to fulfil one of several distinct jobs:

- Peace of mind - the background certainty that a financially catastrophic event won’t ruin them

- Family protection - the assurance that loved ones are financially secure if something happens to them

- Compliance - meeting a requirement set by a mortgage provider, employer, or regulator

- Risk management - making a business or personal exposure manageable

- Financial recovery - the capacity to return to their previous situation after a loss

The problem is that insurance is also one of the most paradoxical products in existence: you buy something hoping you never have to use it. The product experience is almost entirely negative. Premiums leave your account every month. The moment of actual value delivery, the claim, typically arrives in a moment of stress, loss, or crisis. And at purchase, you are asked to pay real money today for abstract future protection against a risk you are biologically wired to underestimate.

Insurance is the only product that is doing its job when the customer never has to use it. And that makes it the hardest product in the world to design well.

The protection gap - the difference between what people have insured and what they actually need insured - is not evidence of irrationality. It is a JTBD failure. The product fails to fulfil the job well enough at the moments that matter. As I describe in The Art of Designing Behaviour (2024): “What people say and what people do are two fundamentally different things.”[6] Customers say they want to be protected. But the moment of buying, the moment of renewal, the moment of updating after a life event - none of these are designed to actually fulfil the job.

Why insurance needs behavioural design

Traditional insurance product development assumes that customers who understand a policy will make rational coverage decisions. If they know what they’re covered for, they’ll choose the right level. If they understand the risk, they’ll take prevention seriously. If the claims process is fair, they’ll file promptly.

This is the rational customer assumption. Behavioural science has spent five decades demonstrating that it doesn’t hold.

Kahneman and Tversky showed that people are systematically more sensitive to losses than to equivalent gains, a principle they called loss aversion.[7] In the insurance context, this means that the immediate, certain cost of a higher premium is psychologically heavier than the uncertain future benefit of better coverage. Weinstein (1980) documented optimism bias: the human tendency to systematically believe that unpleasant events are less likely to happen to them than to others.[8] Customers who intellectually understand that house fires happen genuinely believe, at a deeper level, that their house won’t burn down.

Tversky and Kahneman (1981) also demonstrated how the way risk is presented radically affects behaviour, independent of the objective facts.[9] “You are covered up to £250,000” and “your current coverage would leave you £47,000 short of rebuilding your home” describe the same situation. Customers respond to them completely differently.

And then there is present bias: the preference for immediately available benefits over future ones, even when the future benefits are rationally larger.[10] Premiums are a certain cost today. Claims are an uncertain benefit at an unspecified future point. Prevention programmes fail for the same reason: the effort of prevention is now, the benefit of avoided loss is distant and abstract.

Customers don’t underinsure because they’re careless. They underinsure because the product is designed for rational actors who don’t exist.

This is what behavioural design addresses: not by simplifying the policy wording (though that helps), but by redesigning the moments, defaults, and environments where insurance decisions are made. As I put it: “Influence is far more judo than karate. In judo, you work with the force of your opponent. You take the force that comes at you and try to turn it in a way that works in your favour.”[6] Redesigning insurance behaviour doesn’t mean persuading people. It means structuring the environment so that the desired behaviour is the easiest one.

Three insurance challenges that behavioural design solves

Challenge 1: the coverage gap nobody knows they have

You bought your home ten years ago for £320,000. Your policy covers rebuild costs of £280,000, the figure calculated at onboarding. Construction costs have risen 35% since then. If your house burns down today, you receive £280,000 and need £378,000. The £98,000 shortfall comes out of your pocket.

This scenario plays out for millions of policyholders. At SUE, we worked with a large European insurer concerned about underinsurance in their home products. Nearly 40% of their residential policyholders had significant coverage gaps: the rebuild value on their policy hadn’t been updated in five or more years, while construction costs had risen substantially. The insurer had sent renewal communications flagging this. They had provided online calculators. They had included coverage review prompts in their app. Customers still didn’t update.

The problem was not awareness. It was optimism bias combined with present bias: a house fire is something that happens to other people, and the cost of higher premiums is real and immediate. The rational case for better coverage was clear. The psychological case was not being made.

Challenge 2: the claims experience that destroys trust

Your car has been broken into. Rear window smashed, sat-nav stolen. You call your insurer. You begin your explanation defensively: “I had the car locked properly.” You haven’t even filed the claim yet and you’re already justifying yourself. That feeling - that you need to prove you’re not lying - is precisely what most claims processes generate.

At SUE, we worked with an insurer who wanted to understand why customers were churning at higher rates after a loss event. Interviews revealed something striking: customers who had filed their claim successfully and been fully paid out still left. Not because of the payout. Because of how the claims process felt. Adversarial. As if they were suspects. “They treated me like a potential fraudster” was a recurring theme.

Lemonade, the US-based insurer, built their entire model around redesigning this experience. Rather than treating claims as the moment to apply maximum scrutiny, they designed for the majority of honest claimants: a 90-second AI claims handler, instant payment for small claims, transparent processes. What Lemonade also did: unclaimed premiums are returned to charities that customers choose at year’s end.[11] This actively signals that the insurer is on the customer’s side, not against them. Lemonade’s retention rates significantly outperformed industry averages. This was not a product innovation. It was a behavioural design intervention.

Challenge 3: the prevention programme nobody follows

You receive an email from your health insurer: “Join our prevention platform and live healthier!” You open it. You close it. The next day it’s forgotten. This experience repeats itself for millions of policyholders at every insurer that invests in prevention communication.

At SUE, a health insurer asked us to increase preventive health behaviour among their insured population. Earlier campaigns had generated almost no engagement. Our diagnosis was clear. Present bias always works against prevention: the effort is now, the reward is abstract and distant. You cannot beat present bias by offering better information. You can only beat it by connecting immediate rewards to the desired behaviour.

The model that changed this thinking is Vitality, launched by Discovery Health in South Africa and now operating across multiple markets under various insurer partnerships. Vitality’s insight was simple: prevention behaviour requires immediate rewards, not abstract future savings on claims that may never happen. Cinema tickets for gym visits. Premium discounts for health assessments. Cashback for healthy food purchases. Present bias wasn’t fought. It was redirected.

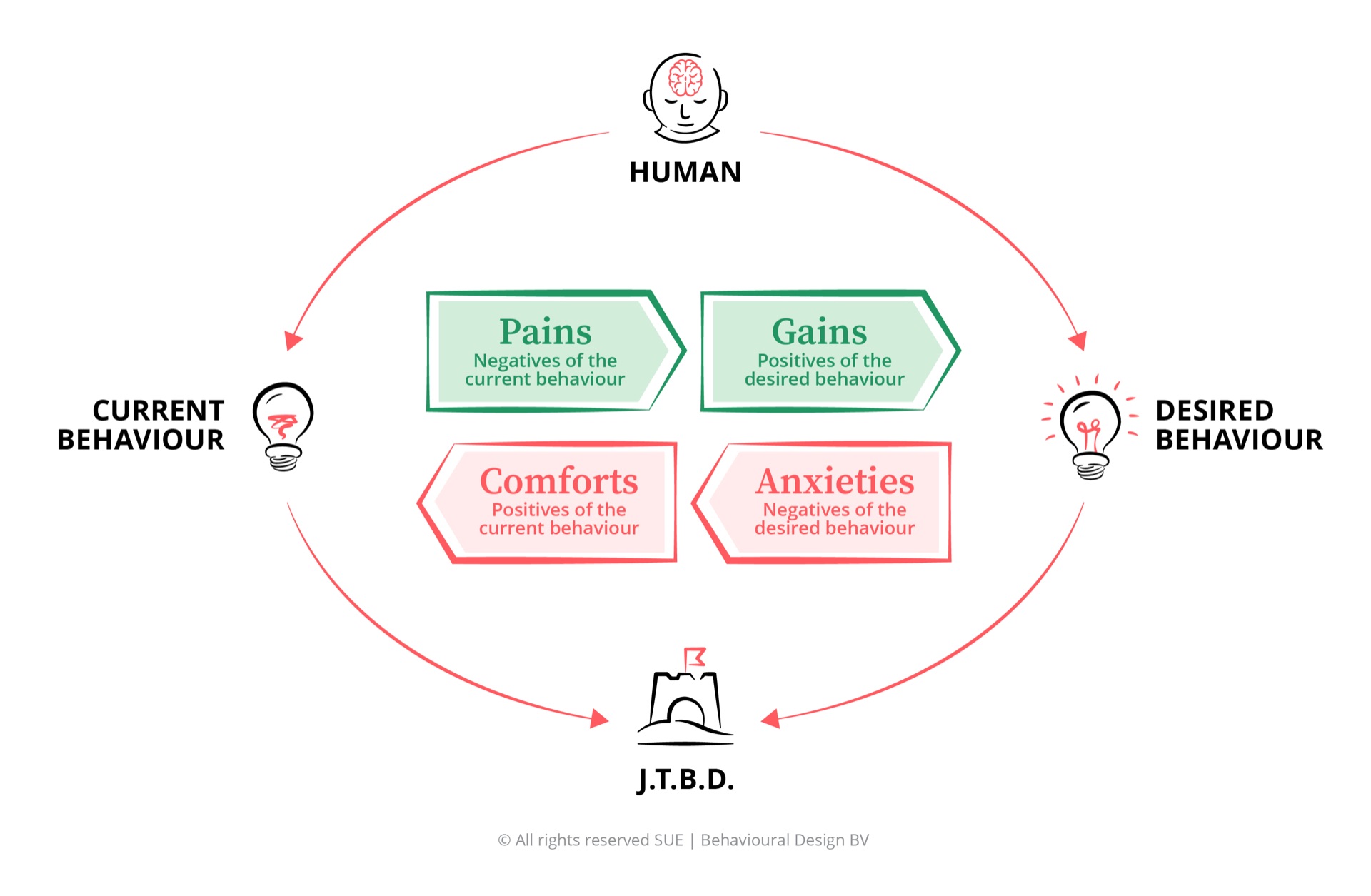

Influence Framework analysis: what drives and blocks insurance behaviour

The SUE | Influence Framework© always starts with the customer’s Job-to-be-Done, because behaviour is never arbitrary. It is always an attempt to make progress in a specific circumstance. For insurance customers, that job is almost always one of three things: financial recovery after loss, peace of mind that loved ones are protected, or the ability to take risks without existential danger. Anyone who understands that underlying job also understands which forces drive behaviour and which ones block it.

Applied to insurance, a consistent pattern emerges: the blocking forces are more powerful than the driving forces, and they are almost entirely unaddressed by standard insurance marketing and product communication.

Why customers underinsure and churn despite understanding the risk

Insurance communication addresses the driving forces effectively. Customers understand the product, understand the risk, and understand the price. What remains unaddressed are the blocking forces: the deep comfort of the current policy and the immediate anxiety about higher premiums that make adequate coverage feel like an unnecessary expense. The customer’s JTBD - peace of mind, family protection, financial recovery - is rarely facilitated at the moments that actually matter.

High churn despite competitive pricing: Insurers lose customers at renewal even when they are price-competitive. The customer doesn’t perceive meaningful differentiation between products, so price becomes the only deciding factor. This is a design failure, not a pricing failure. Products that feel undifferentiated create customers who comparison-shop at every renewal. The JTBD of peace of mind is nominally claimed by every product and convincingly delivered by none.

Low cross-sell and upsell rates: Most insurers have extremely low success rates on cross-sell and upsell across product lines. Customers who trust their insurer for one product don’t automatically extend that trust to other products. The journey from single-product to multi-product - the journey that fulfils the JTBD of integrated risk management - is not designed.

Delayed claims causing larger payouts: When customers delay filing claims, small insurable events become large ones. A water leak reported immediately costs a fraction of one discovered three months later. The financial incentive to encourage prompt reporting is enormous, but almost no insurer designs the customer journey to make reporting feel easy and welcome.

Higher retention through trust: Customers who trust their insurer have materially higher retention rates and are significantly more likely to cross-buy. Trust is built in the claims moment. Insurers who invest in redesigning the claims experience build retention that no loyalty programme can replicate. The claims moment is when the JTBD of financial recovery is truly put to the test.

Lower claims costs through prevention: Programmes like Vitality demonstrate that prevention-engaged policyholders have measurably lower claims costs. The return on prevention programme investment is real, but it requires designing for immediate behavioural motivation rather than abstract future risk. Simplicity - making the prevention behaviour as easy as possible - does more than information campaigns.

Increased coverage per customer: A customer with adequate coverage is better protected and less likely to dispute a claim. Closing the coverage gap is not only an ethical obligation; it is a commercial one. Under-covered customers are dissatisfied customers when they claim. The JTBD of financial recovery is fulfilled. Or failed.

“The current policy is fine”: Customers default to the comfort of the policy they already have. Status quo bias is one of the most powerful forces in insurance behaviour. The effort required to evaluate and update coverage feels disproportionate to the abstract risk. The policy in place feels adequate even when it is not. Johnson and Goldstein (2003) demonstrated this mechanism compellingly in their organ donation research: opt-in countries had registration rates of 4–27%, opt-out countries had rates up to 99.98%.[12] The default is the most powerful design decision an insurer can make.

Risk models work on aggregate: Actuarial models are excellent at predicting aggregate risk. This creates an institutional comfort with the status quo: the portfolio is managed mathematically, and behavioural considerations feel soft and unmeasurable by comparison. This comfort prevents investment in customer journey redesign.

Traditional marketing drives acquisition: Marketing budgets are oriented toward acquisition because acquisition is measurable. Customer journey redesign is a longer-term retention play that requires different investment logic and different success metrics. The comfort of existing measurement frameworks keeps organisations in the status quo.

Higher premiums feel like certain losses: Loss aversion means that the immediate, certain cost of a higher premium is psychologically more salient than the uncertain future benefit of better coverage. Kahneman and Tversky showed that the pain of loss is roughly twice as powerful as the equivalent gain.[7] Customers know intellectually that they should increase coverage. The emotional weight of paying more today for a benefit they hope never to use makes it feel like a bad deal.

Claims anxiety and distrust: A significant proportion of customers delay or avoid filing legitimate claims because they fear their insurer will reject the claim, raise their premium, or find a reason to dispute. This claims anxiety is a direct result of the industry’s reputation for adversarial claims handling. It is not irrational. It is a learned response to decades of claims friction. And as long as the JTBD of peace of mind is not fulfilled at the claims moment, trust is eroded at every interaction.

Prevention programmes feel surveillance-like: Telematics, smart home sensors, health tracking: the prevention technologies that insurers most want to deploy feel intrusive to customers. The anxiety about being monitored and having data used against them is a genuine barrier to programme adoption, even when the financial incentives are attractive.

The key insight: Insurance marketing overwhelmingly targets the driving forces: explain the product, price it competitively, remind customers of the risk. But customer behaviour is determined by the blocking forces, which operate below the level of rational product evaluation. The comfort of the current policy and the anxiety about higher premiums are not overcome by better policy documents or sharper pricing. They are overcome by redesigning the customer journey so that adequate coverage, prompt claims, and prevention behaviour are each made easier, more immediately rewarding, and more socially normal than the alternatives. “You don’t change behaviour by working at the behaviour itself.”[6]

Five behavioural interventions for insurance

-

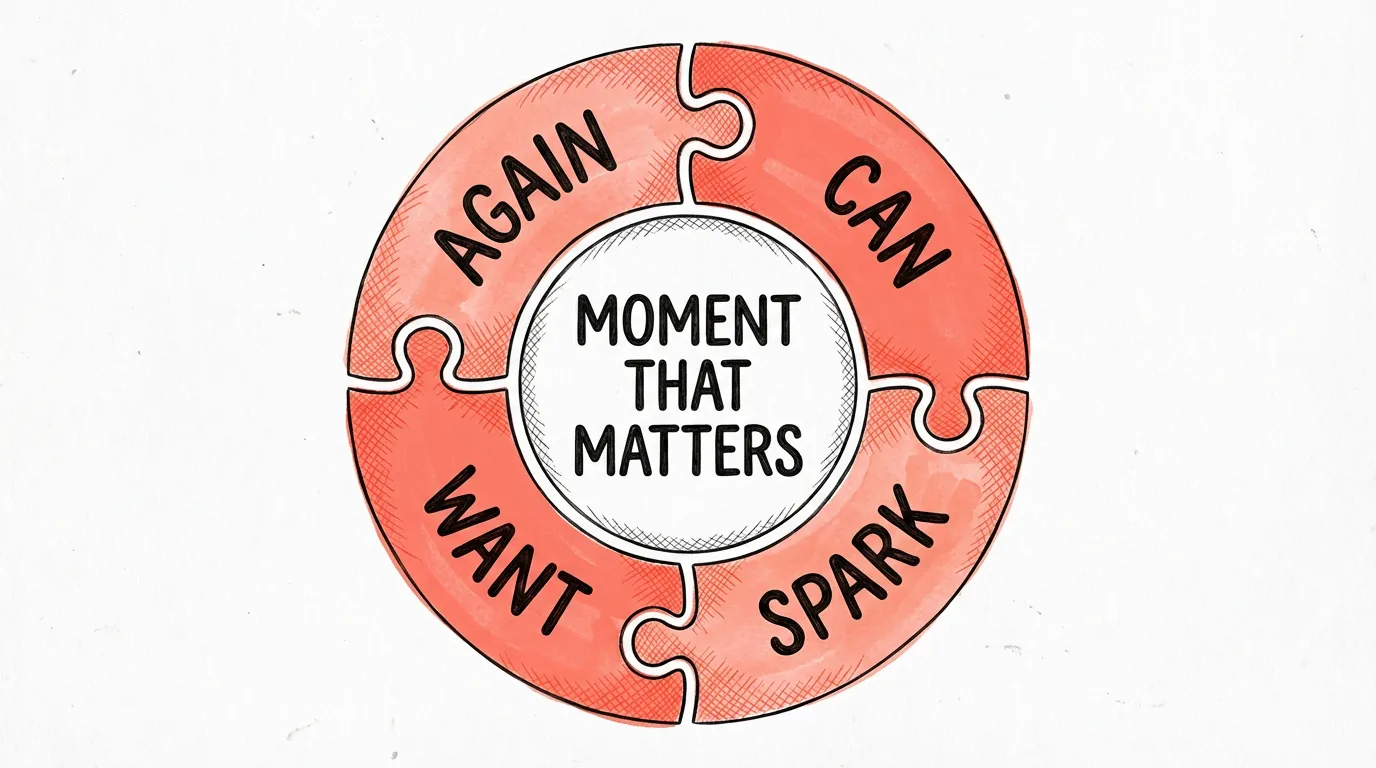

Smart defaults at life events (C01 Default + SPARK)

The highest-leverage moments for coverage decisions are not renewal dates. They are life events: buying a house, getting married, having a child, purchasing a new car. At each of these moments, the customer’s risk profile changes significantly and their attention is already on a major financial decision. Smart default systems that automatically recalculate and present updated coverage at these moments, with opt-down rather than opt-up as the default, close coverage gaps without requiring customers to initiate a review they would otherwise never start. The organ donation research from Johnson and Goldstein demonstrates unambiguously how powerful this mechanism is: the default determines the behaviour of the large majority.[12] In insurance this works identically: requiring opt-down rather than opt-up structurally reduces the protection gap.

-

Loss-framed risk communication (W14 Loss Aversion + W11 Framing)

The framing effect has one of the strongest and most replicated effects in behavioural science. In a classic experiment by Tversky and Kahneman, 72% of participants chose the positively framed option, even though both options were objectively identical.[9] In insurance: “Your current coverage would leave you £47,000 short of rebuilding your home” is more motivating than “upgrading your coverage gives you complete protection.” Both are the same fact. The loss frame activates loss aversion, which is a stronger psychological force than the equivalent gain. Concrete, personalised, in pounds and euros - that’s how it works. Insurers who reframe their coverage review communications around what customers stand to lose consistently see higher review and upgrade rates.

-

Friction reduction in claims (C06 Friction + C22 Prefilling)

The claims experience is the product. Every insurer says this. Very few design accordingly. Friction reduction in claims means: pre-filled forms using policy data the insurer already holds, photo-based first notice of loss for standard damage events, transparent status updates without the customer having to chase, proactive outreach after known trigger events like storms or accidents in the customer’s area. Each friction point removed increases the probability of prompt reporting, which reduces total claims costs and, more importantly, rebuilds the trust that determines retention. The JTBD of peace of mind is only genuinely fulfilled when the claims moment doesn’t feel adversarial. The question is not “how do we prevent fraud?” It is: “how do we design a claims experience that treats honest customers like honest customers?”

-

Immediate rewards for prevention behaviour (W21 Instant Gratification + AGAIN)

Vitality showed what is possible when prevention is designed around immediate rewards rather than future risk reduction. Gym visits earn premium discounts. Health assessments unlock partner benefits. Safe driving earns cashback. The behaviour is prevention. The motivation is immediate gratification. Present bias always works against prevention - unless you shift the reward horizon to the present. Insurers who wait for prevention programmes to justify themselves through claims data over three-year cohorts will always underinvest. The design principle: make prevention immediately and tangibly rewarding, independently of any future claims benefit. The portfolio effect follows.

-

Social norms in coverage decisions (W01 Social proof + W02 Social norm)

People are strongly influenced by what they believe their peers do. Social proof works because it bypasses the rational evaluation that loss aversion and present bias distort, and activates the System 1 drive to conform to perceived norms. “84% of homeowners with properties similar to yours chose to review their coverage after a major renovation” is more motivating than any argument about rebuild costs. Coverage review tools, app prompts, and renewal communications that include peer comparison data consistently outperform those that don’t. The customer doesn’t need to be convinced that they should review their coverage. They need to see that people like them already have.

Which cognitive biases matter most in insurance

Insurance decisions are shaped by some of the most powerful cognitive biases in the behavioural science literature. Here are the five that have the greatest impact on coverage decisions, claims behaviour, and customer retention.

Loss aversion

The psychological pain of losing £100 is roughly twice as powerful as the pleasure of gaining £100. In insurance, this means the certain premium increase feels heavier than the uncertain future benefit of better coverage. Loss-framed communication flips this: show what the customer loses without adequate coverage, not what they gain with it.

Read the full analysis → Behavioural DesignOptimism bias

Most people believe they are less likely than average to experience a house fire, serious accident, or critical illness. This systematic overoptimism is the primary driver of underinsurance. It cannot be overcome by providing more risk statistics. It must be countered by personalised, vivid, concrete loss scenarios that make the risk feel real and proximate.

Read the full analysis → Behavioural DesignPresent bias

Insurance premiums are a certain cost today. Claims are an uncertain benefit at an unspecified future point. Present bias means customers systematically overweight the premium cost and underweight the future coverage benefit. Prevention programmes fail for the same reason: the effort of prevention is now, the benefit of avoided claims is distant and abstract.

Read the full analysis → Behavioural DesignStatus quo bias

The coverage level set at onboarding will persist unchanged for years unless the customer is actively prompted to review it. Status quo bias is why customers who bought a £200,000 home policy ten years ago still have a £200,000 home policy. Smart defaults and life-event triggers are the primary design interventions against status quo bias in insurance.

Read the full analysis → Behavioural DesignFraming effect

“You are covered for up to £250,000” and “your current coverage would leave you £47,000 short” describe the same situation. Customers respond to them completely differently. How coverage gaps, claims decisions, and risk scenarios are framed determines whether customers act or not.

Read the full analysis →Frequently asked questions

How does behavioural design apply to insurance?

Behavioural design for insurance starts with the customer’s Job-to-be-Done: not which policy they buy, but which sense of security they are trying to achieve. Using the SUE | Influence Framework©, you map the four forces that drive and block insurance behaviour: Pains, Gains, Comforts, and Anxieties. You then use the SWAC Tool to design interventions at the exact moments where insurance decisions happen, from onboarding through life events to renewal and claims. You don’t change the customer. You change the environment.

Why do customers underinsure even when they can afford better coverage?

Underinsurance is a behavioural problem, not a financial one. Three forces combine: optimism bias (customers believe bad things are less likely to happen to them than the statistics suggest), present bias (premiums are a certain cost today while claims are an uncertain future benefit), and status quo bias (the coverage level set at onboarding persists unchanged through life events). Customers are not underinsured because they can’t afford better coverage. They’re underinsured because no moment in the customer journey creates the genuine reconsideration that adequate coverage requires.

What is the claims experience problem in insurance?

The claims moment is when insurance becomes real. Most insurers design it for fraud prevention and operational efficiency, creating a high-friction, adversarial experience for honest claimants. Customers delay filing because they anticipate rejection. Documentation requirements feel overwhelming. Timelines are opaque. This erodes trust precisely when trust matters most. Behavioural design redesigns the claims journey to treat honest customers like honest customers: reduced friction, transparent timelines, proactive outreach after trigger events. The result is prompt reporting, lower total claims costs, and dramatically higher customer trust.

How does the SUE Influence Framework work in insurance?

The SUE | Influence Framework© maps four forces for any insurance behaviour: Pains (churn, underinsurance, delayed claims), Gains (higher retention, lower claims costs through prevention, increased coverage per customer), Comforts (the current policy feels adequate, status quo is comfortable), and Anxieties (loss aversion about higher premiums, claims anxiety, surveillance concerns about prevention technology). In insurance, the blocking forces almost always dominate. That is why competitive pricing alone cannot solve retention, and why better policy documents alone cannot solve underinsurance.

What insurance companies use behavioural design?

Several insurers have applied behavioural design principles with measurable results. Vitality (Discovery Health) built a complete prevention ecosystem around immediate rewards. Lemonade redesigned the claims experience from the ground up: claims handled in 90 seconds, instant payouts for small claims, and unclaimed premiums returned to charities customers choose. Centraal Beheer built a brand personality that reduces claims anxiety through approachable, human communication. At SUE we work with insurers across Europe on coverage decisions, claims journey redesign, and prevention programme uptake.

PS

I’ve worked with insurance organisations for years, and the frustration is always the same. Excellent products, sophisticated risk models, and customers who still don’t do what makes sense. The problem is never the product. The problem is that insurance is designed for a rational customer who sits down, reads their policy carefully, and makes an informed coverage decision. That customer doesn’t exist.

The customer who does exist hired your insurance to achieve peace of mind. To protect their family financially. To recover after a loss. Those are their jobs-to-be-done. And as long as you don’t design a single moment where that job feels concrete, personal, and urgent, they will remain underinsured with you and call a competitor after their first real claim.

Once you start designing for that customer - with smart defaults, loss framing, and a claims experience that treats people like people - the numbers move. That is what we do at SUE, and what I describe in The Art of Designing Behaviour (2024). Insurance doesn’t need better policies. It needs better behavioural design.