What Is Behavioural Finance? The Psychology Behind Financial Decisions

The financial sector spends billions on products, advice and communication. And yet: households consistently save too little for retirement, investors sell at the bottom of every crash, advisers miss warning signs in client conversations, and risk committees make decisions that later seem inexplicable.

The problem is the assumption, not the products.

The financial industry is built on the premise that people are rational actors. That they objectively weigh risk, prioritise long-term interests over short-term gratification, and translate information into sound decisions. Decades of research prove the opposite. People are not homo economicus. They are predictably irrational, in ways we can now describe with precision. That is what behavioural finance is about.[1]

Behavioural finance is an academic field that studies how psychological biases and cognitive patterns influence financial decision-making - from individual investors to boardrooms. The field proves that people are not rational financial actors but predictably irrational beings who systematically deviate from classical economic models. More on how behavioural science works in marketing and finance →

What is behavioural finance?

Behavioural finance is the field that studies the psychology of financial decisions. It combines insights from cognitive psychology with financial economics to explain why people systematically deviate from what rational choice theory predicts.

The field begins in 1979, when Daniel Kahneman and Amos Tversky published Prospect Theory.[2] Their central finding: people weigh losses psychologically more heavily than equivalent gains - roughly twice as heavily. This sounds simple. The implications are enormous. It means a portfolio is managed differently when it is "in loss" than when it is "in profit", even at identical absolute values. It means framing determines whether someone buys insurance. It means the order of information changes an investment decision.

Richard Thaler - who received the Nobel Prize in Economics in 2017 - translated this to financial markets.[3] He showed that stock exchanges behave as collective psychology, not collective rationality. Robert Shiller proved that stock prices systematically deviate from fundamental values, precisely because investors behave like humans.[4]

Today behavioural finance is no longer a niche. It is an established field with dedicated chairs, professional programmes and applications at banks, insurers, regulators and pension funds worldwide.

Why classical financial advice fails

Classical financial advice is built on a model: inform the client about risks and returns, provide objective data, and the client will make a sound choice. This model fails systematically, because the brain simply does not work that way.

Take pension saving. Dutch and British households consistently know they save too little for retirement. Research shows roughly 80% acknowledge this. And yet a large proportion does nothing. This is the gap between knowing and doing: information changes knowledge, but knowledge alone does not change behaviour.

Or take investor behaviour during a market downturn. Rationally, a long-term investor would stay calm during a correction - or even add to positions. In practice, a large group of investors sells at exactly the lowest point. The availability heuristic makes recent losses hyperpresent in the mind. Loss aversion triggers panic. And the pain of loss - which weighs twice as heavily as the pleasure of gain - overwhelms any rational long-term calculation.

"Influence is far more judo than karate. You work with the forces already present, and redirect them in the direction you want."

The same applies on the supply side. Banks and insurers still design most of their communication, product pages and advice sessions around information transfer. More charts, better graphs, clearer brochures. While the real problem is the context in which decisions are made.

The 7 psychological barriers in financial behaviour

In masterclasses for financial professionals - at banks and insurers including KBC, Rabobank, ABN AMRO and Allianz - I encounter the same seven patterns every time. They are predictable, which means they are also designable.

1. Present bias: the pension savings trap

The brain values now over later. Considerably more. Economists call this hyperbolic discounting: an amount received today feels psychologically heavier than the same amount in five years. For pension saving, this means someone rationally knows they should save more, but the signal "pension" simply does not feel urgent. Thirty years is too far away for System 1. The result: procrastination, the feeling that it "can wait", while time passes irreversibly.

2. Loss aversion and the availability heuristic

Losses feel twice as heavy as equivalent gains. This sounds theoretical but is measurable in every investment portfolio. After a market crash - or even after prominent media coverage of losses - people dramatically overestimate the risk of investing. The availability heuristic amplifies recent examples: "I know someone who lost everything in 2008." That mental availability overrides statistics, return history and objective probability calculations.

3. Status signalling

Money is not only used to build wealth. It is used to communicate social status. An expensive car, a luxury watch, a larger home than needed - these are all investments in social identity, not in financial capital. Financial professionals who ask "why don't you put this aside?" do not understand what they are asking. They are asking someone to give up a social signal. That does not come easily.

4. Hyperbolic discounting in saving

Closely related to present bias, but distinct. In hyperbolic discounting, the discount people apply to future rewards is not linear but steep. A reward of £1,500 in two years feels less attractive to many people than £1,000 now - even though £1,500 is objectively better. This is not irrationality. It is an evolutionary survival mechanism that has little affinity with modern financial planning.

5. Happiness illusions and financial consumerism

People consistently overestimate how much happiness a purchase will bring. This is called focal thinking: we focus on the pleasure of ownership and ignore the adaptation that quickly follows. The new house, the new car, the holiday - within months it has become normal. But the mortgage, the lease payment, the credit card debt remains. Financial products that exploit this mechanism play with a vulnerability, not a need.

6. FOMO and herd behaviour

The rise of crypto, the popularity of certain stocks, word of mouth about "that one investment" - this triggers what behavioural scientists call social proof and FOMO. When people in your circle are making money, not participating feels dangerous. This is exactly the mechanism that fuels bubbles: people buy high because others expect further rises. And sell low because the herd panics. The availability heuristic amplifies this: stories of people who won big are shared more widely than stories of loss.

7. Digital temptation

Contactless payment, buy-now-pay-later, the disappearance of physical money - this lowers the psychological threshold for spending. The pain of paying - a real phenomenon that research repeatedly confirms - is minimised by digital payment methods. There is no longer a moment of resistance. You tap, you click. The expenditure feels like less of a loss. This is not an accidental by-product of fintech. For some players, it is a designed feature.

Groupthink in the boardroom: behavioural finance at organisational level

Behavioural finance is not only about individual customers. In workshops with risk committees, compliance teams and executive boards at financial institutions, I see the same biases - but collectively amplified.

Confirmation bias in risk assessment. Risk committees reviewing a file unconsciously seek information that confirms their initial judgement. A corporate client who has been in the books for twenty years as "good risk" is assessed differently from a new client with identical financial ratios. The relationship history colours the assessment. This plays out in property portfolios, credit assessments and AML decisions.

The HIPPO effect. In every meeting with a clear hierarchy, the Highest Paid Person's Opinion dominates. Other participants adjust their views. Through a combination of authority bias, confirmation and social conformity, without being aware of it. The result is that the committee's risk perception reflects the risk perception of the highest-ranking person in the room - not the collective analysis.

Sunk cost in strategic decisions. "We have invested ten years in this system, we cannot stop now." This is the sunk cost fallacy in its purest form. Organisations hold on to systems, portfolios and relationships not because it is rational to continue, but because the accumulated investment has psychologically acquired a value of its own. This plays out in AML software, corporate banking relationships and IT migrations.

Optimism bias in forecasts. Business plans that boards must approve are systematically too optimistic. Not because the authors are incompetent, but because people consistently overestimate the probability of positive outcomes and underestimate the probability of negative ones. Combined with commitment escalation - the feeling that you have come so far - this leads to decisions that later seem inexplicable.

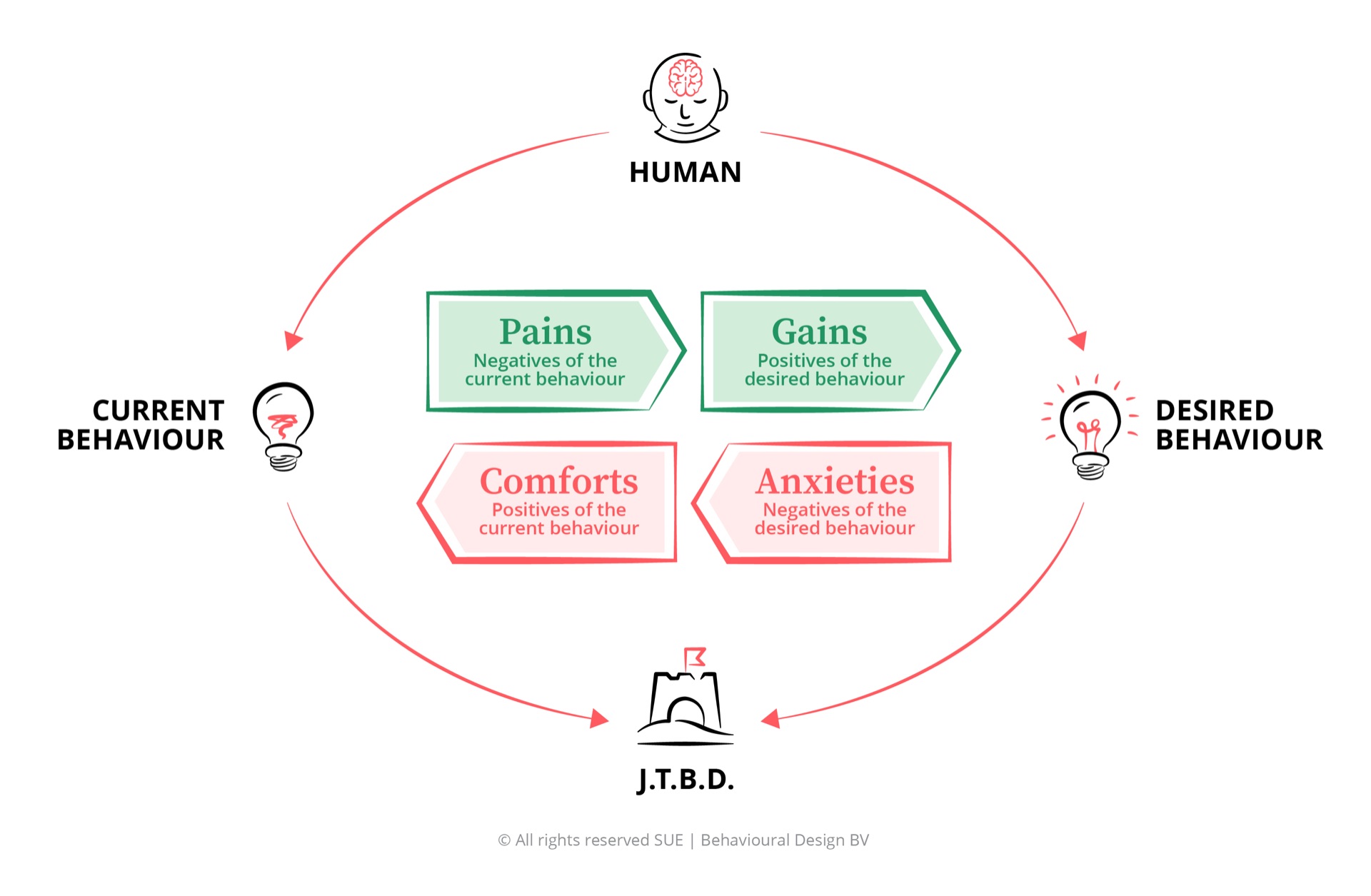

The SUE Influence Framework applied to finance

To work effectively in the financial sector - whether as product designer, communications professional, adviser or compliance manager - you need a tool that maps the psychology behind financial behaviour systematically. The SUE Influence Framework is designed for that.

Take the example of someone who saves too little for retirement. The standard approach: inform this person about pension gaps, show charts, explain the importance. The behavioural finance approach starts with the Influence Framework:

- Job-to-be-Done: "Feeling financially secure" or "having the freedom to do what I want later", not just "pension saving". This is the real underlying motivation.

- Pains: The feeling that money is always tight. Shame about lack of financial overview. Fear that saving yields little at low interest rates.

- Gains: Peace of mind, freedom, security. The feeling of doing the right thing for your future self. Control over the future.

- Anxieties: "I don't know how much I need." "The pension system is so opaque." "I can't miss that £50 per month right now." These are the real barriers - not lack of information.

- Comforts: Current spending patterns feel fine. Spending money now gives immediate satisfaction. Procrastination is comfortable as long as the problem remains abstract.

When you know these forces, you can redesign the experience. ING did this with a single question: when signing up for a pension plan, participants were asked to concretely imagine what their life would look like if they retired comfortably. One concretisation question. The result: 20% more enrolments.[1]

That is the result of working with the brain rather than against it.

Behavioural finance in practice: what you can do tomorrow

The question financial professionals most often ask me after a masterclass: how do I actually apply this? Three levels of application.

Product design and choice architecture. Defaults are the most powerful tool in financial product design. In countries where pensions are automatically arranged (opt-out), participation is 80-90%. In opt-in countries, it is 15-30%. Same people, same pensions, different defaults. If you want to change customer behaviour, you start with the default, not with the campaign.

Client communication and advice. Loss frames work more powerfully than gain frames. "What does it cost you if you don't do this?" activates loss aversion - a force twice as strong as the attraction of gain. This is not manipulation if it is true. An adviser who says "at your current trajectory you will face a shortfall of £350 per month in retirement" speaks to a different force than "with this product you could build an additional £350 per month". Both are true, but only one activates the brain.

Risk governance and decision-making. Pre-mortems are the most underused technique in financial organisations. Before a major decision - an acquisition, a credit extension, a system investment - the team imagines the project has already failed. "It is two years from now and it went completely wrong. What happened?" This breaks confirmation bias and groupthink, because System 1 is asked to construct a negative scenario rather than seek confirmation.

Frequently asked questions about behavioural finance

What is the difference between behavioural finance and behavioural economics?

Behavioural economics is the broader science studying how psychology influences economic behaviour across all domains: health, education, energy, work. Behavioural finance is its application specifically to financial markets and decisions: investing, saving, risk management, insurance and financial advice. All behavioural finance is behavioural science, but not all behavioural science is behavioural finance.

Who founded behavioural finance?

The scientific foundation was laid by Daniel Kahneman and Amos Tversky, who published Prospect Theory in 1979. Richard Thaler (Nobel Prize in Economics 2017) developed the field further with mental accounting and nudging. Robert Shiller (Nobel Prize 2013) showed that stock markets are systematically mispriced due to psychological factors. Werner De Bondt and Thaler published the first direct evidence in 1985 that stock markets overreact to news.

What are the most important biases in financial behaviour?

The most researched are: loss aversion (losses weigh twice as heavily as gains), present bias and hyperbolic discounting (preference for immediate rewards), status quo bias (avoiding action is the default), availability heuristic (overweighting recent events), confirmation bias (seeking evidence that confirms existing views), and groupthink in collective decision-making. They overlap, reinforce each other, and occur in combination.

How do banks use behavioural finance in product design?

The most direct application is choice architecture: the way options are presented. Automatic enrolment in savings plans (opt-out rather than opt-in), displaying comparison options that make the desired choice more attractive, concretisation questions in financial advice, and framing risk as "chance of loss" versus "chance of gain" are all behavioural science applications. Some are ethical and work for the client. Others are ethically questionable and work for the bank. The distinction matters.

What is mental accounting?

Mental accounting is a concept by Richard Thaler: people divide their money mentally into separate "pots" with different rules. A tax refund feels different from salary, even at an identical amount. "Holiday money" is spent differently from regular pay. A bonus goes more easily towards a luxury purchase than savings. This has major implications for product design: how you label and present money influences how it is spent.

1.5 minutes of Influence

Join 6,500+ readers · Free · Unsubscribe anytime