Mental Accounting Explained: Why You Keep Money in Separate Mental Buckets

Suppose you receive a tax refund of 600 euros. And shortly afterwards an unexpected bill for the same amount. Objectively, they cancel each other out. But that is not how it feels. The tax refund felt like a windfall. The bill felt like a loss. The money is identical, but the mental processing is worlds apart.

Or consider a bonus payment. That same amount landing in your account as salary and there is a good chance you put it aside or spend it sensibly. As a bonus? It goes more readily towards a holiday, a new bicycle, or a nice dinner out. It just feels different. Like "extra".

This is mental accounting: the phenomenon that Nobel laureate Richard Thaler described as one of the most predictable deviations from rational financial behaviour.[1]

Mental accounting is the psychological phenomenon whereby people unconsciously divide their money into separate mental "buckets", each with its own rules about how that money can be spent or saved. Developed by Richard Thaler (Nobel Prize in Economics, 2017): a bonus feels different from salary, a tax refund different from savings - even when the amounts are identical. Mental accounting explains much financial behaviour that classical economics calls "irrational" but which is, in reality, predictable and systematic. More on behavioural science in financial services →

What is mental accounting?

Classical economics rests on a simple principle: money is fungible. One pound is one pound, regardless of where it came from or what it was earmarked for. A rational actor treats savings, salary, tax refunds and bonuses as a single total and allocates it optimally across expenditures.

People do not do this. They divide their money into mental categories - buckets, in effect - and apply different rules to each. A pound in the "holiday fund bucket" behaves differently from a pound in the "emergency reserve bucket", even when both sit in the same bank account.

Richard Thaler documented this systematically in his paper Mental Accounting Matters (1999) and later in his popular book Nudge (2008, with Cass Sunstein).[2] His central observation: people encode, categorise and evaluate financial outcomes differently from what an objectively rational model would predict. And they do so in recognisable, predictable ways.

Thaler distinguished three core aspects of mental accounting:

- How are income and expenditure encoded? Gains and losses are felt differently from what objective figures suggest.

- How are money flows categorised? Which mental bucket does an amount end up in, and what rules govern it?

- How frequently is the balance assessed? Daily, monthly, per transaction - the frequency determines how loss aversion manifests.

Amsterdam

Amsterdam

Rated 9.3 out of 10. Certificate included.

Three forms of mental accounting that shape your behaviour

Mental accounting manifests in three ways that appear repeatedly in financial behaviour, both among consumers and inside organisations.

1. Labelling: the bucket determines the rules

When money receives a label, it behaves differently. "Holiday money" goes more readily towards a luxury purchase than regular wages. "Savings for the children" remains untouched even when expensive loans are outstanding elsewhere. A "tax refund" feels like a windfall and triggers different spending patterns from regular salary.

A classic finding from the research: people keep savings in a low-interest account while simultaneously carrying credit card debt at high interest. Rationally, this is costly - they should use the savings to clear the debt. But the savings sit in a mental bucket ("for later", "for emergencies") that they do not want to disturb. The credit card debt sits in a different bucket ("everyday spending") with different rules.

Thaler described this as one of the most costly consequences of mental accounting: people carry unnecessary financial burdens to preserve the integrity of their mental buckets.

2. The windfall effect: found money goes faster

Money that arrives "out of nowhere" is treated differently from earned money. A tax refund, a bonus, an inheritance, a prize draw - these amounts land in a mental bucket with looser rules. They feel like "extra", and therefore less costly to spend.

This is the windfall effect, and it has concrete consequences for how financial products and policy work. A tax rebate programme designed to encourage saving works differently when communicated as a "bonus" (spent quickly) rather than as a "withholding reduction" on regular salary (less visible, less quickly spent).

"Money is money - unless it comes from somewhere. Then it is something else."

Thaler and Sunstein described in Nudge how the US tax system activates this mechanism unintentionally: tax refunds are spent more readily than equivalent tax withholding reductions across the year, even when the net amount is identical. The timing and framing of money determine the mental bucket, and the bucket determines behaviour.

3. Payment coupling and sunk costs

Mental accounting also shapes how people deal with what they have already paid. A ski pass costing 160 euros - already paid - generates a strong feeling: "I need to get my money's worth from it." Particularly on a day with bad weather.

In an experiment, two groups of skiers received either a bundled four-day pass (160 euros upfront) or four separate day tickets (40 euros each). On the fourth day - bad weather - the group with individual tickets was significantly more likely to go skiing anyway. Their mental accounting linked each day to a separate payment. That link activates the sunk cost effect: "I have already paid, so I am going."

The group with the bundled pass felt that link less strongly. The payment was "done"; each individual day was mentally separate from it.

This has significant implications for designing subscriptions, memberships and loyalty programmes. Where you want to encourage sustained engagement, visible monthly billing outperforms annual auto-debit: the coupling between payment and use is stronger, and the sunk cost motivation helps. The same principle applies to rent payments - timing collection at or just after salary payment day significantly reduces arrears, because the salary still feels mentally "complete".[7]

Mental accounting in financial services: evidence from the field

Mental accounting is not a theoretical curiosity. The effects have been measured in field experiments with large populations and hard outcome measures.

India: envelopes increase savings fivefold. In a study with households earning the equivalent of £6.60 per week, salaries were not paid as a single lump sum but pre-divided into labelled envelopes: one for food, one for rent, one for the children's education. The education envelope carried a photograph of the family's children. The result: the savings rate rose from 0.74% to 4% of income - a fivefold increase, with the same people on the same income.[3] The envelopes activated mental accounting deliberately: each bucket got a label, and the label protected it against impulsive spending.

UK: savers with a specific goal save 35% more. Research by Cheema and Ulkumen among British savers found that only 28% had a concrete savings goal. That group saved an average of £150 per month. The group without a specific goal saved £111 - 35% less. The same mechanism at work: a label gives money identity, and identity makes it harder to touch.[4]

Bank of America: Keep the Change. Every debit card purchase was automatically rounded up, with the difference transferred to a savings account. Participants needed to do nothing after the initial sign-up. Results following the launch: 12.3 million participants, $2 billion saved, 99% of participants stayed enrolled.[5] The combination of automation and the psychological framing of "change" (a distinct mental bucket) made saving invisible enough not to generate resistance.

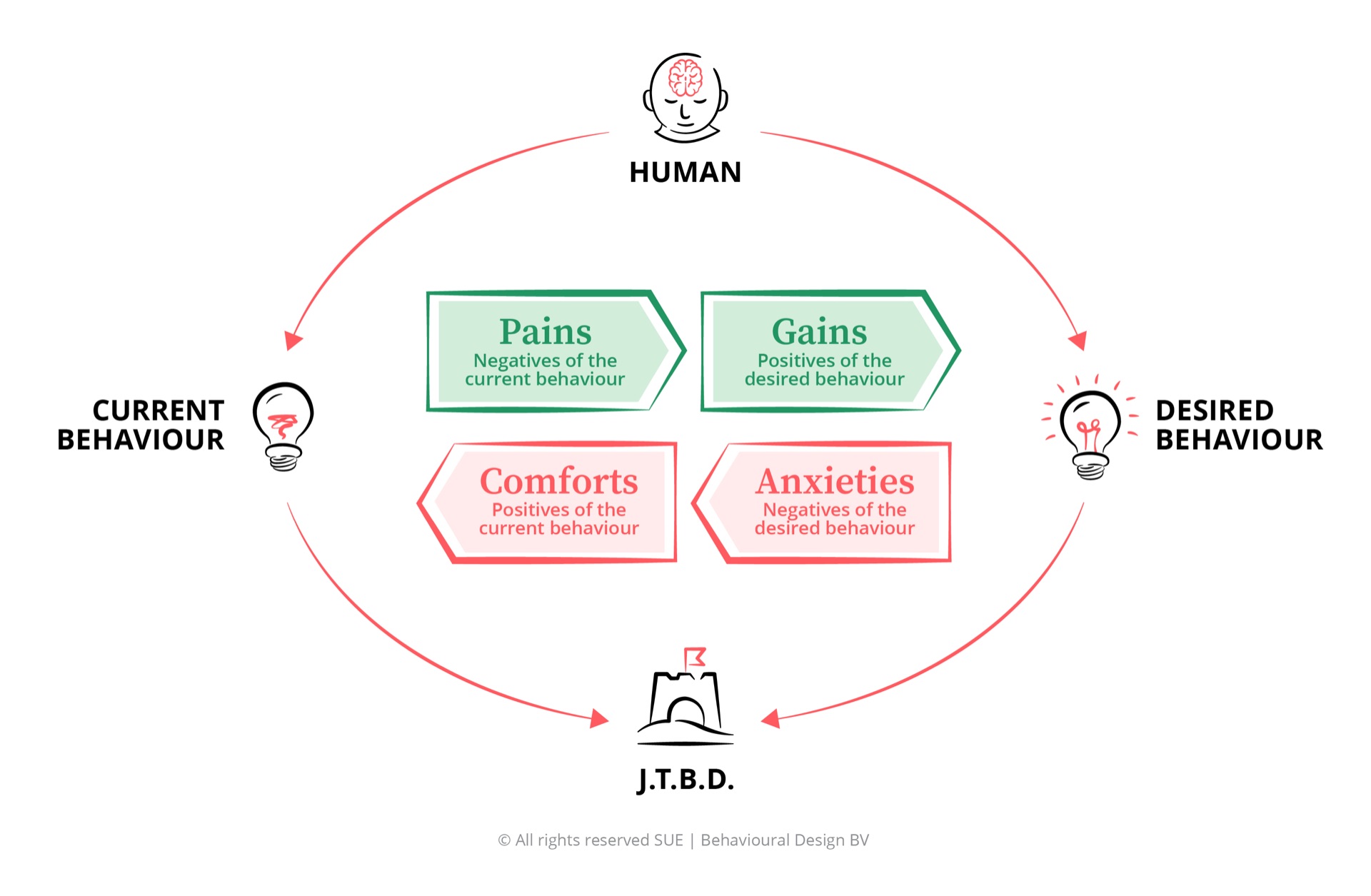

The SUE Influence Framework applied to mental accounting

Mental accounting describes a pattern. To use that pattern as a practitioner - in product design, communication or advice - you need a tool that translates it into concrete design decisions. The SUE Influence Framework does exactly that.

Consider someone who saves too little, while knowing they should save more. Standard approach: inform them about the pension gap, show a graph, give advice. The Influence Framework approach starts by asking: which four forces keep this behaviour in place?

- Pains: The feeling that money is always tight by month's end. A vague anxiety about not having enough later, alongside the very tangible financial pressure of right now.

- Gains: Peace of mind, control, the feeling of doing right by your future self. For some: the sense that putting money aside is also a form of self-discipline that generates quiet pride.

- Comforts: Current behaviour works well enough. Spending money brings immediate satisfaction. Postponement is comfortable as long as the problem remains abstract. And: the mental buckets already in place feel familiar and right.

- Anxieties: "I do not know how much I will need." "If I put it away, I won't have it for unexpected costs." "The pension system keeps changing anyway." These are the real barriers - not a lack of information, but uncertainty anxiety.

Once you know the comforts are this strong, you design differently. ING did this with a single extra question on a pension plan enrolment form: they asked participants to vividly imagine what their life would look like if they retired comfortably. One concretisation question, targeting the gain force. Result: 20% more enrolments, with exactly the same information provided.[6]

That is working with mental accounting rather than against the behavioural pattern.

Using mental accounting in product design and communication

Three design principles that follow directly from Thaler's insights.

Labelling as a design tool. By naming money, you activate mental accounting deliberately. Modern banking apps do this with savings buckets: a pot for the holiday, one for a car, one for unexpected costs. The money sits in the same account, but the label makes it psychologically untouchable for other purposes. Rabobank, ING and various fintech players apply this. The underlying psychology is consistent: labelled money is spent less readily.

Framing new income. How you present an amount determines which mental bucket it lands in. A pay rise communicated as an "annual bonus" goes more quickly towards luxury spending than the same rise framed as a structural salary component. If you want people to manage a particular sum sensibly, frame it as regular income or goal-directed savings - not as a windfall.

Payment timing and coupling. When a payment happens relative to consumption determines how visible costs feel and how strong the sunk cost motivation is. For behaviour you want to sustain, visible monthly billing outperforms annual auto-debit: the link between payment and use is stronger, and the sunk cost drive helps. For behaviour you want to reduce, bundling payments and decoupling them from individual decisions weakens the sunk cost pull.

Frequently asked questions about mental accounting

What is mental accounting?

Mental accounting is the psychological phenomenon whereby people unconsciously divide their money into separate mental "buckets", each with its own rules about how it can be spent or saved. Developed by Richard Thaler, it describes why objectively identical money is treated differently depending on its source, label or context. A bonus feels different from salary. A tax refund feels different from savings. That felt difference drives concrete behaviour.

Who developed the concept of mental accounting?

Richard Thaler, economist at the University of Chicago and Nobel Prize laureate in Economics (2017). His key paper is Mental Accounting Matters (1999). Thaler built on Kahneman and Tversky's earlier work on prospect theory and loss aversion, and translated it into concrete financial behaviour patterns. His book Nudge (with Cass Sunstein) brought the concept to mainstream audiences.

What are concrete examples of mental accounting?

The most recognisable: a tax refund more often goes towards a luxury purchase than towards paying off debt, even though it is objectively the same money. A bonus goes more readily towards a holiday than salary does. "Holiday pay" feels different from regular wages. People hold savings in a low-interest account while carrying credit card debt. Shares "sitting at a loss" are held in the hope of recovery, even when that is not rational. All of these patterns are consequences of mental buckets with their own rules.

How does mental accounting differ from loss aversion?

Loss aversion describes how people weigh losses more heavily than equivalent gains - the pain of loss is roughly twice as powerful as the pleasure of a gain. Mental accounting describes how people categorise money and apply different rules per category. They interact: money in a mental bucket feels like "owned", making its loss extra painful. But they are two distinct mechanisms. Loss aversion explains how strongly something is felt; mental accounting explains which rules apply per category.

How can mental accounting be applied in financial product design?

By deliberately labelling and partitioning money you activate mental accounting by design. Savings buckets in banking apps - a pot for a holiday, one for a car, one for emergencies - use this principle. Bank of America's "Keep the Change" programme rounded up every purchase and transferred the difference automatically to savings. The label "change" made it psychologically easier not to spend it. General principle: give money a name and a purpose, and people protect it better.

1,5 minutes of Influence

Join 6,500+ readers · Free · Unsubscribe anytime