The Psychology of Risk: Why We Systematically Misjudge Risk

Imagine two scenarios. In the first, you toss a coin. Heads: you win 200 euros. Tails: you lose 100 euros. Expected value: positive. Yet the majority of people refuse to play this game.[1]

In the second, you choose between a certain gain of 500 euros or a 50% chance of 1,000 euros. Most people take the certain gain, even though the expected values are equal. But flip the choice to losses - a certain loss of 500 euros versus a 50% chance of losing 1,000 euros - and suddenly the same majority does take the gamble.

There is a fundamental inconsistency in human risk behaviour here: we are risk-averse when it comes to gains, and risk-seeking when it comes to losses. We gamble to avoid loss but not to achieve gain. This is not irrational behaviour in the popular sense. It is systematic, predictable and robustly demonstrated across cultures, ages and contexts.

Risk perception is the subjective assessment people make of the likelihood and severity of a negative outcome. It deviates systematically from objective probability: loss aversion, the availability heuristic and emotional framing drive the judgement more than statistics do. Kahneman and Tversky showed that people do not calculate risk but feel it, and that this skews in predictable ways. More on behavioural science in financial services →

What is risk perception?

Risk perception is not the same as risk calculation. An actuary calculates risk using probabilities and outcomes. A person experiences risk through their feeling system, their memory, their fears and their social environment. Those two rarely converge.

Classical economic models assumed people are rational risk assessors: given probabilities and outcomes, they maximise expected utility. Reality is radically different. People judge risks relative to a reference point, not in absolute terms. They are guided by how vivid a risk is in their mind, not by how probable it is. And they respond asymmetrically to losses and gains.

This has significant consequences for every field that deals with decisions: from pension advisers to insurance products, from investment communications to compliance. If you do not understand risk perception, you design financial products and communications for a human who does not exist.

Prospect theory: how we actually experience gains and losses

The most influential theory about how people experience risk and value is prospect theory, developed by Daniel Kahneman and Amos Tversky in 1979.[2] They formulated three insights that overturned the classical expected utility model.

Insight 1: reference points, not absolute values. People do not judge outcomes in absolute terms ("I have 950 euros") but as gains or losses relative to a starting point ("I have lost 50 euros"). The same end figure feels completely different depending on where you started. This makes communicating financial outcomes fundamentally different: the framing of the reference point determines the felt value.

Insight 2: asymmetric sensitivity. The value function in prospect theory is S-shaped. For gains, the pleasure diminishes quickly: the difference between 0 and 100 euros feels larger than the difference between 900 and 1,000 euros. For losses, the same pattern holds, but in the negative direction. And the crucial point: the loss curve is steeper than the gain curve. Losses weigh psychologically roughly twice as heavily as equivalent gains.[3]

Insight 3: risk error patterns are predictable. People are systematically risk-averse for gains (take the certain outcome) and systematically risk-seeking for losses (gamble rather than face certain loss). This pattern is part of what makes behavioural finance such a powerful lens: human irrationality is not random noise but structured and foreseeable.

"Losses hurt roughly twice as much as gains feel good. This is not a weakness - it is how the human brain is built."

The practical implication for financial services: products that communicate risk purely through expected returns reach System 2 (the rational thinker). But purchase decisions are made by System 1 (the intuitive feeler). The framing of loss and gain around a reference point determines the emotional response, and that emotional response determines behaviour.

Amsterdam

Amsterdam

Rated 9.3 out of 10. Certificate included.

Five ways risk perception systematically skews

Loss aversion is the most well-known mechanism, but risk perception skews in several ways. For anyone designing or guiding financial decisions, five patterns are especially relevant.

1. Loss aversion. Already described: losses weigh more heavily than equivalent gains. The practical consequence: investors hold loss-making positions for too long (realising the loss feels worse than holding paper losses), and take profits too early (fear of losing the gain outweighs the potential of further growth). This pattern is called the disposition effect and is one of the most extensively documented errors in investor behaviour.[4]

2. Status quo bias. The current situation serves as the reference point. Any change relative to the status quo is framed as a loss, even when the change is objectively better. This explains why people stay with poor pension arrangements, switch too rarely to better savings products and fail to cancel unfavourable insurance policies. Inertia is not laziness; it is the logical outcome of loss aversion combined with reference point thinking.

3. Availability heuristic. How vivid a risk is in memory determines how large people estimate it to be. After a plane crash, people overestimate the risk of flying. After news of a bank failure, demand for cash rises. After a long period of economic growth, investors underestimate downside risk. Availability in memory does not correlate with statistical probability - but it does correlate with fear response.

4. Optimism bias. Most people believe negative outcomes are more likely to happen to others than to themselves. Some 80% of drivers believe they drive better than average, around 90% of entrepreneurs believe their business will succeed despite statistics suggesting otherwise, and most adults estimate their chance of serious illness as lower than actuarial tables justify. Optimism bias is evolutionarily explicable but financially costly: it leads to insufficient savings buffers, too little insurance and too little risk diversification.

5. Illusion of control. People rate risks as lower when they feel they have personal influence over the outcome. An investor who manages their own portfolio experiences the risk differently from a passive fund investor, even with identical risk profiles. A driver experiences risk as lower than a passenger does. A sense of control reduces the fear response, regardless of whether that sense of control actually influences the outcome.

Risk perception in financial practice: what research shows

These mechanisms are not laboratory curiosities. They have been measured in field studies with large groups and hard outcome measures, and have been consistently demonstrated in the financial sector.

UK: a photo of your own car doubles compliance. The British government sent letters to owners of unlicensed vehicles: "Pay your tax or lose your [make of vehicle]." Limited effect. But when the letter included a photo of the specific car owned by the recipient, compliance increased significantly.[5] The risk was identical: loss of the vehicle. But the photo activated loss aversion by making the loss concrete and personal. Abstract probability plus a felt sense of personal ownership is a very different experience from abstract probability alone.

Stickk.com: putting money at stake works. The commitment platform Stickk (set up by Yale economists Dean Karlan and Ian Ayres) lets users stake money on personal goals. If they miss their weekly goal, the amount goes to a cause they hate - an "anti-charity". Result: 50 million dollars at stake, 521,000 completed commitments, 40 million cigarettes not smoked.[6] The anti-charity maximises loss aversion: not only financial loss but identity loss too (you support something you abhor).

ING: a single concretisation question increases pension enrolment by 20%. In a field experiment, ING added a single question to a pension plan enrolment form: asking participants to vividly imagine what their life would look like if they retired comfortably. No additional information. No financial advice. Just a concretisation question that made the abstract future loss (insufficient pension) vivid and felt. Result: 20% more enrolments, with exactly the same information provided.[7] The availability heuristic works in both directions: make the desired scenario vivid, and people act on it.

The pattern across all three cases is the same: not more information, but better activation of the feeling layer. Making risk concrete, personal and vivid does more than calculating it accurately. Understanding this is central to behavioural design for financial services.

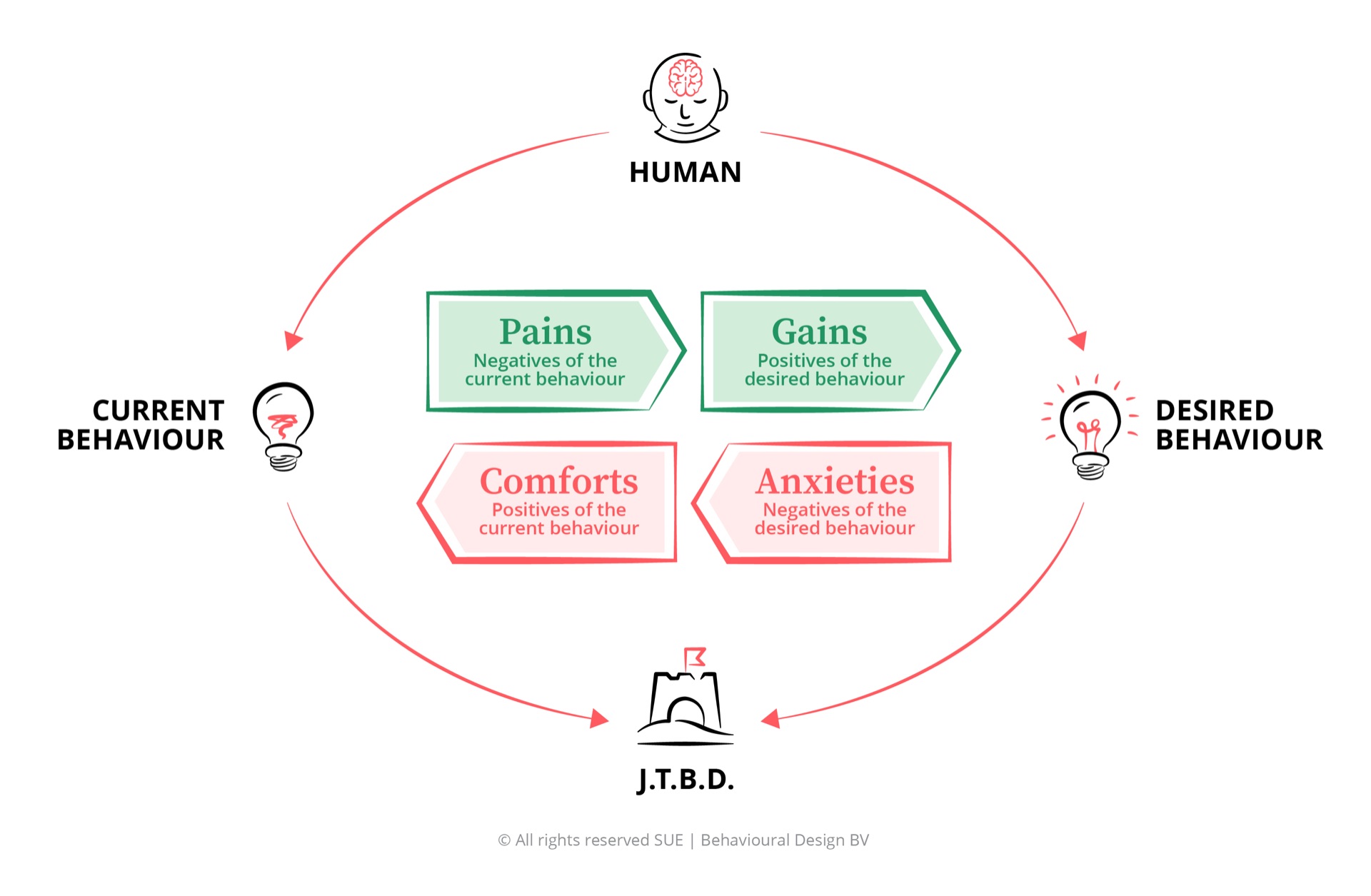

The SUE Influence Framework applied to risk decisions

To translate risk perception into concrete design decisions you need a tool. The SUE Influence Framework makes visible the four forces that maintain any behaviour - including risk behaviour.

Take someone who has held a loss-making investment position for years and will not sell. Classic approach: inform them, show the numbers, advise them to rebalance. The Influence Framework analysis asks first: which four forces maintain this behaviour?

- Pains: The feeling of losing control over the situation. The thought that they misjudged it. Social loss: others seeing they were wrong.

- Gains: If they hold the position, there is still a chance of recovery. The loss is on paper, not realised. Hope is a powerful gain.

- Comforts: Doing nothing costs no effort. The current situation is the reference point. "I have not really lost it as long as I do not sell."

- Anxieties: If I sell and it recovers afterwards, I will have realised a loss for nothing. I do not know what else to do with the money.

The comforts and anxieties are dominant here - they maintain the behaviour even when rational analysis points the other way. A good adviser or a well-designed product does not work by reinforcing the pains and gains (yet more information about why selling is sensible), but by removing the anxieties. Concretely: an alternative that is immediately and easily available at the decision moment reduces the fear of the empty gap after the sale.

This is the core of behavioural science in financial services: not pushing harder, but removing barriers. The logic of loss aversion cannot be argued away, but it can be reframed or circumvented. More on this in our article on mental accounting, which shows how the same money feels completely different depending on how it is labelled.

How to design with risk perception

Four design principles that follow directly from the psychology of risk.

1. Frame loss, not gain, when you need urgency. Loss framing activates System 1 more strongly than gain framing. "You are missing out on 23,000 euros of pension savings by not enrolling now" is more activating than "You can build 23,000 euros by enrolling." Use this with care and ethical awareness - but use it, because it works.

2. Make the abstract loss concrete and personal. The UK car letter case shows this: the same message, but with a photo of the recipient's specific car, worked far more effectively. Personalise the risk. Make it visible, tangible, yours. "Your pension gap" works better than "the average pension gap." "Your home" works better than "property value."

3. Use commitment devices that activate loss aversion. Let people put something concrete at stake: time, money, reputation. That raises the cost of non-performance. Pre-commitment - specifying in advance what you are going to do - uses loss aversion as an ally. Mental accounting plays a role here too: money that has already been labelled as savings feels like a loss if spent.

4. Neutralise status quo bias with easy defaults. If the current situation is the reference point, any deviation from it feels like a potential loss. The way to break through that is to make the desired behaviour the default. Automatic pension enrolment works not because people are more motivated, but because the status quo is now "enrolled" rather than "not enrolled." Defaults are the most powerful single intervention in behavioural design, precisely because they flip loss aversion in favour of desired behaviour.

Frequently asked questions about the psychology of risk

What is risk perception?

Risk perception is the subjective, psychological assessment people make of the likelihood and severity of a risk. It deviates systematically from objective probability through loss aversion, the availability heuristic, optimism bias and emotional framing. Kahneman and Tversky showed that we do not calculate risk but feel it - and that this skews in predictable ways.

What is prospect theory and why does it matter for financial services?

Prospect theory (Kahneman & Tversky, 1979) describes how people subjectively experience outcomes: as gains or losses relative to a reference point, not in absolute terms. Losses weigh psychologically roughly twice as heavily as equivalent gains. For financial services this is fundamental: it explains the disposition effect in investors (holding loss-making positions too long), low pension participation, insufficient insurance uptake and irrational reactions to market volatility.

How does loss aversion work in financial decisions?

Loss aversion means the pain of loss is stronger than the pleasure of an equivalent gain. In financial behaviour this shows as: investors holding loss-making shares to avoid realising the loss, consumers not switching to better mortgage deals because switching feels risky, and savers taking too little risk in their pension portfolio because the chance of nominal loss weighs more heavily than the chance of return. See also what is behavioural finance for the broader context.

Why do rational risk communication and financial advice work so poorly?

Because they address System 2 (the rational, deliberating thinker) while risk decisions are largely made by System 1 (fast, intuitive, feeling-driven). A chart showing expected returns reaches the intellectual judgement but not the feeling system. Effective risk communication makes the risk concrete, vivid and personal, so that it is also emotionally felt by System 1.

What is the availability heuristic and how does it affect risk perception?

The availability heuristic is the tendency to estimate the probability of an event based on how easily an example comes to mind. Vivid, recent or emotionally charged events feel more probable than they statistically are. After a market crash, people overestimate downside risk. After a long bull market, they underestimate it. Risk communication that activates vivid images - including positive future scenarios - influences risk perception more strongly than abstract statistics.

1,5 minutes of Influence

Join 6,500+ readers · Free · Unsubscribe anytime